All the biggest, blue-chip companies of today started out as the small start-ups of yesterday. Some created entirely new industries, such as Google and Netflix, or changed them significantly, such as Tesla and rivian, Most, if not all, became the names we recognize today through equity-based compensation, enriching their founders, executives and early employees alike (along with investors). A major part of equity compensation, especially for first-stage companies, is incentive stock options (ISOs).

Incentive Stock Options (ISO) – Defined

ISO gives employees the right, but not the obligation, to purchase company stock at a lower-than-expected grant price.[1], compared to the fair market value (FMV) at the point of future exercise. This difference between a higher FMV and a lower grant value at exercise is called bar profit element, If the value of the element of the deal is positive, the option is said to be “in the money”. ISOs are valued not only by the extent of the bargaining element, but also by the potential of the underlying stock. continue to increase in value over time, In other words, the full value of ISO is its intrinsic value, or how much it is “in the money”, plus its time value remaining until expiration.[2] Finally, ISO, like all options, has implied leverage whereby a change in the price of the underlying stock causes a greater change in the value of the option.

How do companies use ISOs?

ISOs are often part of a pre-IPO company’s compensation package because issuing them conserves cash, which can be a scarce resource, and is a valuable employee retention and motivation tool. A typical vesting program for an ISO grant is over four years with a 1-year cliff. With this schedule, 25% of the shares are vested after the first year (this is the “1-year cliff”) and the remaining 75% vests over the remaining three years, often on a monthly basis. You will have a maximum of 10 years to use the ISO, but usually only 90 days to do so if you leave the company. That 90-day period can be extended, but often requires negotiation by the employee and changes the tax treatment of ISOs.

How is ISO taxed?

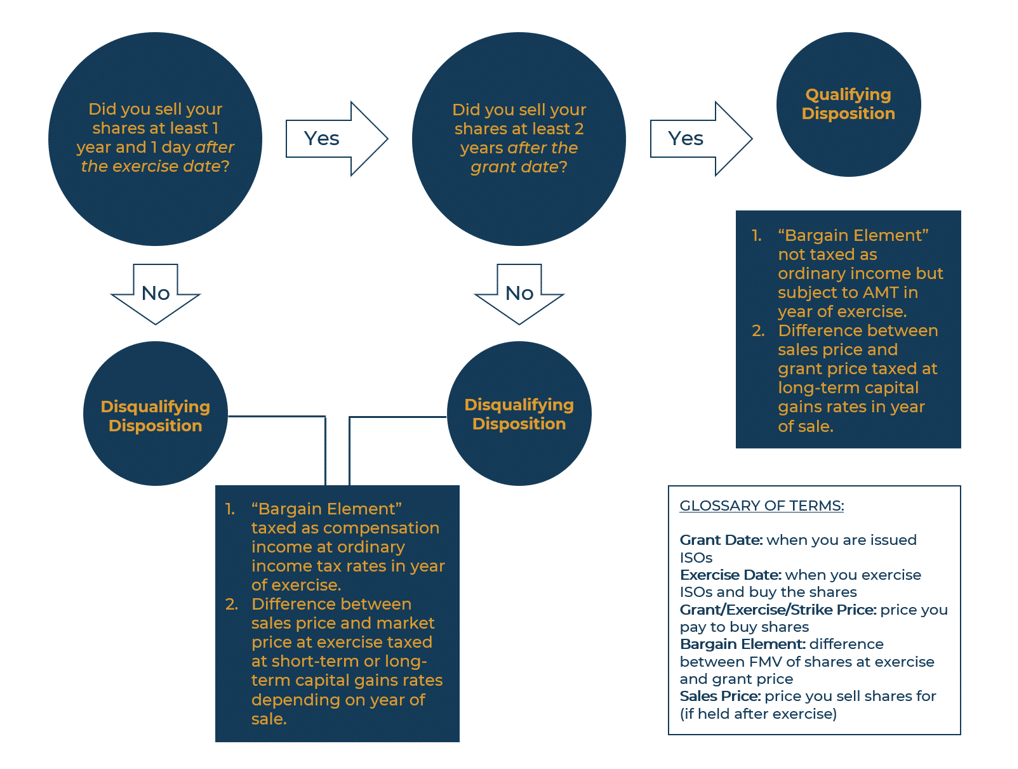

Exercise on ISO is not taxed as ordinary income, but The bargaining element is included as part of alternative minimum tax When the exercised shares are held until the end of the calendar year. The AMT can particularly affect ISO grants for high income earners and those with a large bargaining element. The full tax implications for ISOs depend on whether the exercise and final sale is a “qualifying disposition”, or a “disqualification disposition” as summarized in the flowchart below:

- Feather ‘qualifying temperament’ Is a sale of shares held more than two years after the ISO grant date And One year after the exercise date.

- Feather ‘disqualified nature’ There is any sale of shares that does not satisfy both of the above criteria.

The main advantage of a qualifying provision for ISO is that (1) the bargaining element is not taxed at federal ordinary income rates – as much as 37% – (2) but is instead taxed, as well as any Even after the appreciation exercise, the preferential long-term capital gains rate at between 15-20% (plus 3.8% if net investment income tax applies). This can lead to a higher total profit after-tax balance due to the positive arbitrage between the ordinary and capital gains tax rates. Still, a qualifying disposition comes with significant cash flow implications and risks.

The main advantage of a qualifying provision for ISO is that (1) the bargaining element is not taxed at federal ordinary income rates – as much as 37% – (2) but is instead taxed, as well as any Even after the appreciation exercise, the preferential long-term capital gains rate at between 15-20% (plus 3.8% if net investment income tax applies). This can lead to a higher total profit after-tax balance due to the positive arbitrage between the ordinary and capital gains tax rates. Still, a qualifying disposition comes with significant cash flow implications and risks.

Qualification vs. ineligibility disposition – cash flow

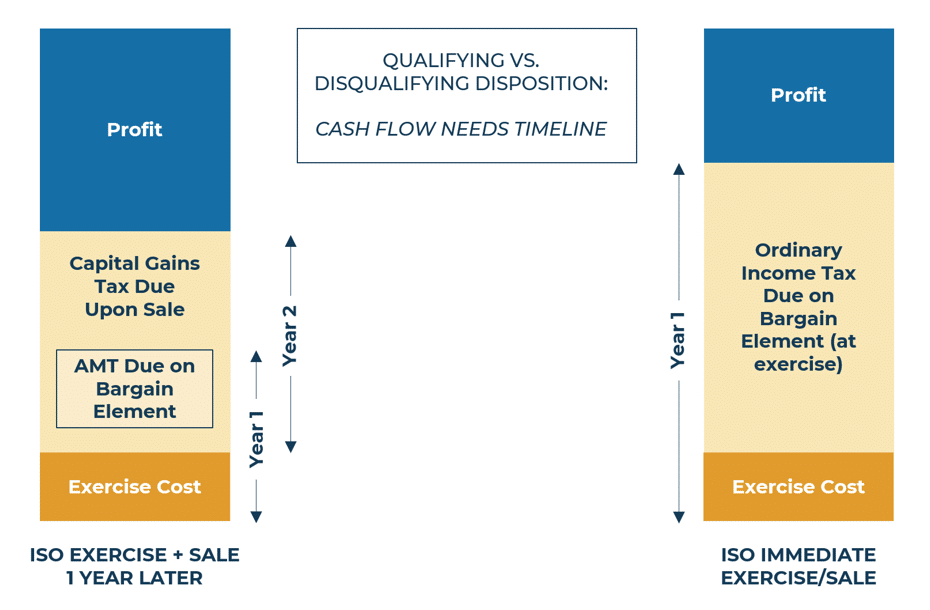

Below is an example of a timeline for an ISO qualifying disposition (left) compared to an unqualified disposition (right). Note that the left side assumes the shares are exercised in Year 1, then sold the following year after all holding requirements are met, versus the right side which assumes a full sale immediately upon exercise in Year 1.

While the illustration is an over-simplification, it does clarify the cash flow requirements and the timeline for the tax benefits of the qualifying provision:

While the illustration is an over-simplification, it does clarify the cash flow requirements and the timeline for the tax benefits of the qualifying provision:

Qualifying disposition – exercise and sell 1 year. Later

- Exercise Cost – (Granted Value x Number of Shares exercised) payable in Year 1

- The shares must be bought on their own. This cost can be significant, and the cash must come from outside sources if the shares themselves are not sold to provide liquidity.

- AMT payable on ISO bargaining element – (AMT tax rate x bargain element) in year 1

- Generally, the AMT rate is 26-28%, but most taxpayers receive an AMT exemption amount that reduces liability. Still, for ISOs “in the money”, this bill could be significant.

- The tax will be payable at the next year’s tax filing deadline.

- long term capital gains tax [(sales price – grant price) x number of shares sold] year 2. payable in

- Thankfully, this can be paid for using share earnings but will be available in a different tax year than the AMT.

- Astute readers may wonder why there appears to be a “double tax” of both the AMT and the capital gains tax. But payment of AMT in Year 1 will generate a credit which can be carried forward and applied to the tax liability payable in Year 2 from the sale of shares.

Disqualification disposition – exercise and sell immediately

- Exercise Cost – Payable in Year 1.

- Again, shares must be purchased first, but immediate sale after exercise in an unqualified disposition provides the necessary liquidity.

- Ordinary income tax payable on transaction element – (federal marginal tax rate x transaction element) payable in Year 1.

- Since the shares are sold immediately, there is no AMT liability, but the shares are now included as compensation income on the W-2 and are taxable at ordinary income rates. It will typically pay higher total taxes than a qualifying disposition.

last words of caution

It is important to emphasize that while a qualified disposition of ISO will often yield the most tax-efficient results, it is not without risk and may very well not be the right choice for you, so consult with your accountant or tax attorney. Counseling is important. About your specific situation. During the year between practice and sales, the holder is fully exposed for the investment risk of the underlying stock. It increases if he is relying on selling the shares in the next year to get capital gains tax treatment and pay the AMT tax due from the previous year. What happens if the share price falls? The holder may not have the requisite liquidity to pay the tax.

Using an ISO late in a calendar year without selling shares can compound these issues, potentially leading to an AMT tax bill only a few months later in April. This may increase the need to sell shares earlier than otherwise planned. Importantly, a qualifying disposition does not need to be an all-or-nothing judgment. Some ISO shares can be exercised and held while sold immediately enough to cover the estimated tax bill. Selling shares to cover the cost of an ISO exercise can be a viable option but is complicated or unavailable for pre-IPO companies.

Finally, companies are not required to withhold taxes for employees when using ISO, no matter what the ISO disposition. And while there is no federal income tax liability due to the exercise, if the AMT is due, it could lead to some unpleasant surprises next year. It would be prudent to consult a tax advisor to make quarterly estimated tax payments to increase W-2 withholding or to offset additional tax due. If this is not done, you may face a hefty underpayment tax penalty.

Conclusion

Most employees who have ISOs often have other forms of equity-based compensation such as non-qualified stock options (NQSOs), restricted stock/restricted stock units (RSUs), and/or employee stock purchase plans (ESPPs). Incorporating these into a comprehensive equity liquidation and tax planning strategy that considers your financial goals important and is part of what Wealthspire Advisors does for our clients. Contact Today.