A reader asks:

Why are we where we are with the total market cap on GDP (Buffett Indicator) and tell me what this could mean going forward?

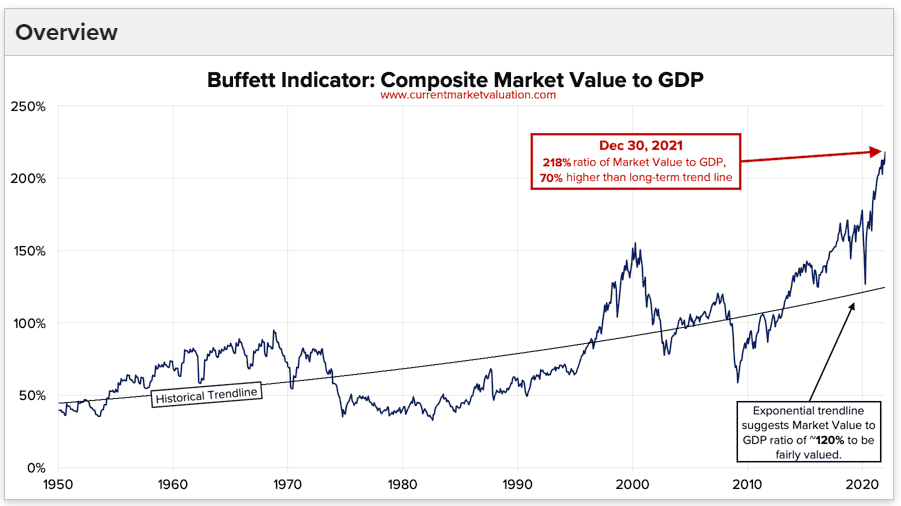

The Buffett indicator was born in a 2001 Fortune interview between the Oracle of Omaha and Carol Loomis. It simply compares the market capitalization of the US stock market to US GDP.

Here’s what Buffett had to say at the time:

There are some limitations to the ratio in telling you what you need to know. Still, it is probably the best single measure of where the valuation stands at any given time. And as you can see, about two years ago this ratio increased to an unprecedented level. This should have been a very strong warning sign.

That very strong warning sign was when the market cap of GDP reached 150% in late 1999/early 2000.

If that ratio was a strong warning sign, the current valuation level said hold my Cherry Coke:

By today’s measurements, the stock market is the most undervalued of all time. This makes the late 1990s cool by comparison.

So this is the biggest stock market bubble in history, isn’t it?

I think it is possible.

It’s also possible that things change and one number doesn’t tell you everything you need to know about what’s happening in the stock market.

At Berkshire Hathaway’s annual meeting in 2017, Buffett posed a question about the valuation metric that now bears his name along with the CAPE ratio. This was his answer:

Buffett said, “Every number has some meaning.” “It sometimes means more than others. … And the two things you mentioned are very much tied. Not that they are unimportant. … They can be very important Sometimes they can be almost completely unimportant. It’s not as simple as one or two formulas and then saying that the market is undervalued or overvalued.

One of the main reasons Buffett changed his tune was the level of interest rates.

10-year treasure from 1995-1999 when the dot-com bubble exploded in outer space Average 6.1%. Since 2019, the 10-year average yield is just 1.2%. All else equal, a lower discount rate should mean a higher value for the financial assets.

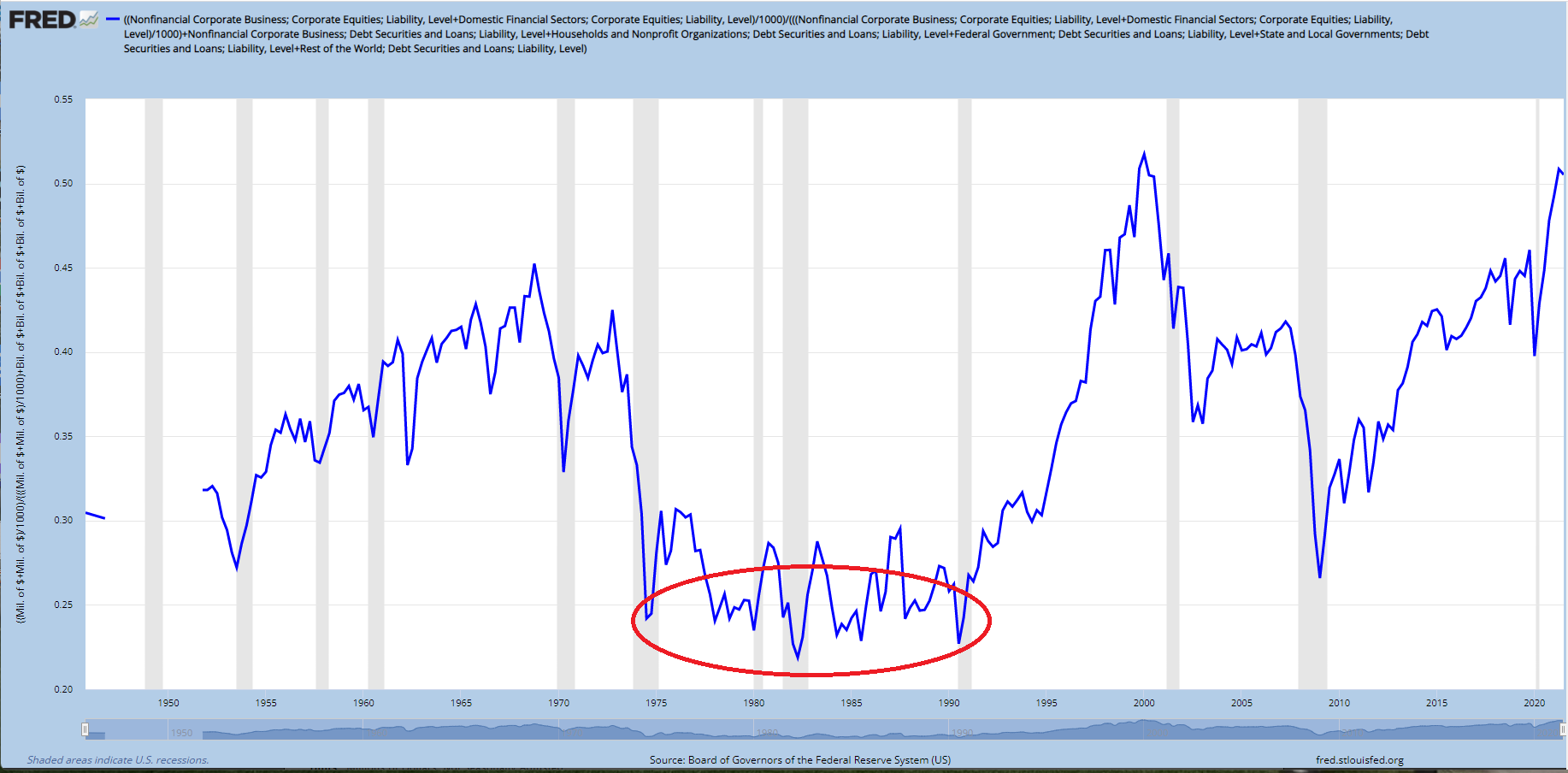

Despite the effectiveness of this valuation measure, the apparent trend is higher in financial assets than in the economy over the past 3-4 decades.

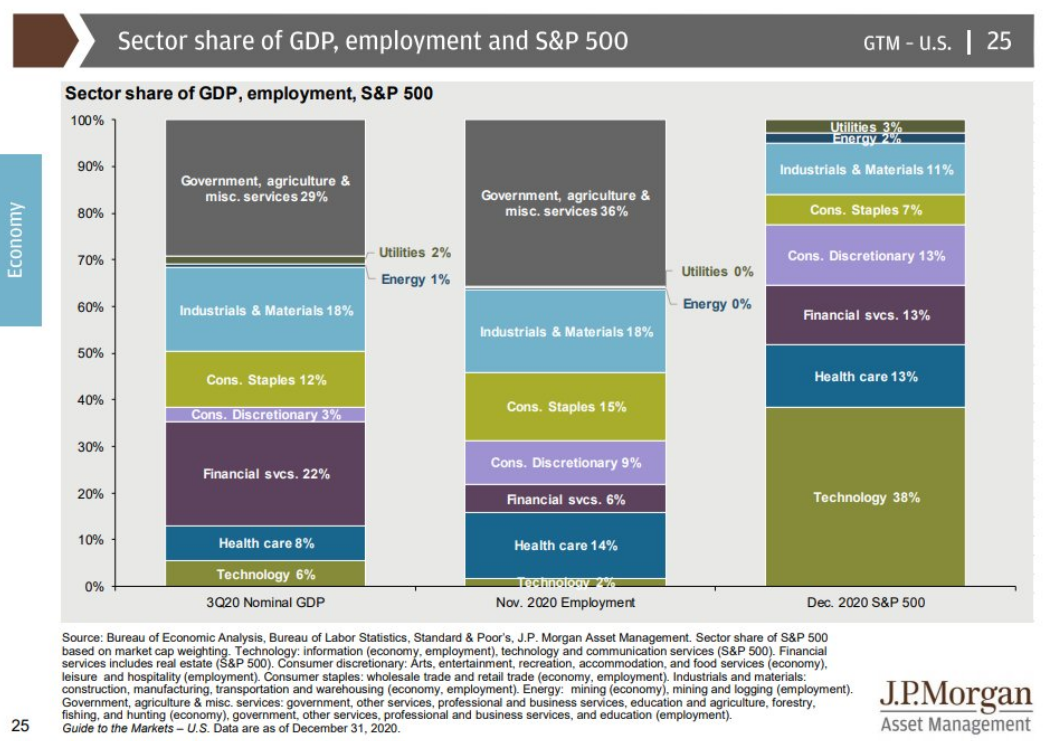

This chart from the JPMorgan Guide to the Markets, which compares the GDP of all US financial assets, makes it even clearer:

How is this even possible?

First, we have stock vs. To clear the flow thing.

Stocks are measured at a specific point in time (that is, the stock market). Flow is measured over a specific time period (economy). Every year the economy is generating trillions of dollars worth while the stock market is a cumulative amount.

So we are in some sense comparing apples to oranges.

We are also just rich as a nation but rich in different ways. In the 1970s and 1980s more money was tied up in private businesses. Now corporations are more ubiquitous. Now you see Starbucks, Target or Walmart in almost every city. Many of them may have been local mom-and-pop stores in the past.

And think about how big companies like Apple, Amazon, Microsoft and Google are. These companies basically now have their own economies and they are global in nature.

Globalization is another trend which has changed the equation here. The Buffett Indicator compares the US stock market capitalization to the US economy. But corporations now get a substantial portion of the business from overseas.

According to my friends at Calcbench, S&P 500 companies now get about 40% of their revenue from countries outside the United States. Apple gets 60% of its revenue from international sources. Amazon is over 40%. For Google, it’s more than half that.

Also think about how easy it is to access the financial markets. See the average household allocation to equities over time:

During the 1970s and 1980s, families owned only 25% or more of their assets allocated to shares. This low allocation came from several factors — very high interest rates (and inflation), terrible market returns in the ’70s, and a lack of useful retirement investment options.

In 1978 Ted Baena accidentally created a 401(k) plan. Now people put a percentage of their paycheck into their workplace retirement plan every time they get paid. It simply did not exist in the past.

And for the last 10 years or so, target debt funds have been the default investment option in most defined contribution retirement plans. These funds now have assets of about $2 trillion and are increasing.

It is easy to invest. It is cheap to invest. We have better technology, lower fees and lower minimums.

It is therefore no surprise that financial assets have grown faster than the economy.

Also a simple fact that the stock market is not an economy:

Technology corporations make up a larger portion of the S&P 500 than the US economy. Government spending makes up a bigger part of the US economy than the US stock market (please, no Fed jokes).

Is the stock at the high end of nearly every valuation metric imaginable?

most likely.

Are things as crazy as they were in 1999?

In some cases yes but overall I don’t think so.

Does it make sense to have context around historical stock market averages and valuations?

Yes, yes it does.

I talked about this question on this week’s Portfolio Hedge:

With some help from my colleague Blair Duquesne, we answered questions about buying or leasing a car, when to contact a financial advisor, and the pros and cons of taking out a 401(k) loan.