By my calculations, the Federal Reserve has raised its short-term benchmark interest rate — the fed funds rate — nearly 100 times since 1970.

It’s actually over 85 or so in that time they lowered interest rates.

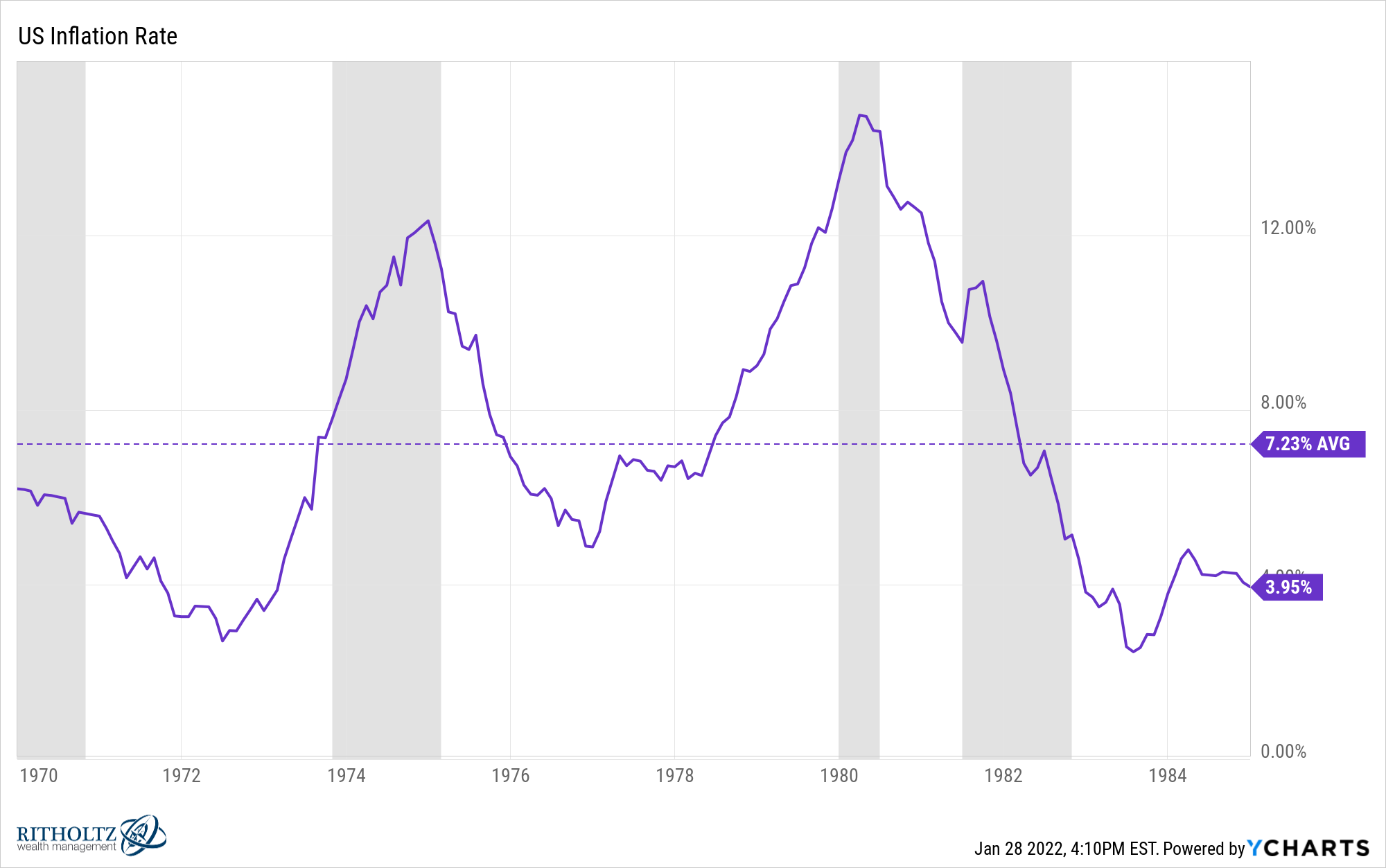

The bulk of those rate hikes occurred between 1970 and 1984 when the Paul Volcker-led Federal Reserve was rapidly raising rates to slow inflation.

In early 1971, short-term rates were less than 4%. By 1981 they had grown to 20%. The Fed wasn’t messing around. By 1984 rates were still close to 12% and did not fall below 5% until 1991.

There’s a reason the Fed spent most of this time tightening monetary policy. Inflation averaged over 7% per year from 1970 to 1984:

This is a period that includes four recessions, two of which were more or less deliberate by the Fed (in the early 1980s).

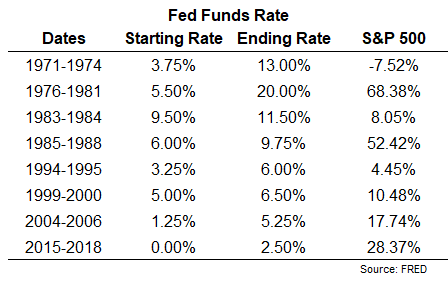

If we break down all these rate increases over time into longer cycles, there really aren’t that many. I count 8 of them since 1970. Here they are with stock market returns during those rising rates environments:

Surprisingly, the stocks have performed relatively well during past hiking cycles. The average total return over these periods was 23%.

However, this data requires a dump truck of salt.

The stock crashed nearly 50% in 1973-74.

The market rose in 1981 but fell 27% in a brutal bear market that extended into 1982 (which included the aforementioned recession induced by the Fed).

The 1985–1988 period includes the biggest one-day crash ever in October 1987, which saw the market fall by 34% in one week.

The sudden rate hike in 1994 shook the bond market as much as the stock market. The S&P 500 had recovered sharply to 8.5% in the early part of 1994, but the overall US bond market (-6.4%) and junk bonds (-7.7%) sold out almost as much.

The fed funds rate remained high for much of the 1990s, but was lowered after the Russian debt crisis of 1998. Rates were raised again in the second half of 1999 after the dot-com bubble burst in the first half of 2000.

The market was halved in the 2000-2002 bear market.

Short-term rates hit their lowest level (at the time) of 1% since the 2001 recession, the stock market crash, and 9/11. Then came the cycle of hiking from 2004-2006. The stock was doing well during this period but peaked 15 months later before the Great Financial Crisis.

After 7 years of 0% rates following the 2008 crisis, the next series of rate hikes began in 2015. When the Fed signaled they would change course, they only gained as high as 2.5% before a near-bear market in stocks on Christmas Eve 2018.

So while the stock market has experienced relatively good returns while the Fed has hiked in the past, the results in and around those hiking cycles haven’t been great.

It makes sense when you think about the reasons the Fed is raising rates. This usually happens when the economy is heating up, speculation is running high or inflation is above trend.

We hit 2 out of 3, which is why the Fed is going to start another series of rate hikes.

I think it’s possible that investors know volatility happens when the Fed raises rates so we’re taking that out for now.

Short-term rates have increased. Speculative stocks have declined and the stock market is in the midst of a minor correction.

And the funny thing is, the Fed hasn’t raised rates yet!

Will it buy them for a while? Will they be patient? Or is the effect of inflation more this time?

I honestly don’t know.

What I do know is that rates are much lower than most hiking cycles in the past, so it’s understandable that investors are nervous.

Think of the stock market like a very, very long term bond.

When dealing with bonds, all else equal, the longer the term, the higher the volatility, both up and down.

That’s why 30-year bonds are seeing a much higher rise in price than 2-year bonds when rates fall. Alternatively, the same 30-year bond will have a much bigger loss than a 2-year bond when rates rise.

And when rates are low, volatility will be high. If the prevailing interest rate is 7%, an increase of 0.25% is relatively modest. But if the market rate is 1%, then a move of 0.25% is proportionately large.

It is not necessarily the end of the world, but it is understandable that volatility has increased.

Will this continue?

Again, I don’t know. I guess it depends on what the price is in the stock market at the moment.

Now it’s not just interest rates that matter in this equation. You can make the case that it is inflation that is the biggest driver of volatility this time around.

And in my next part, I’ll do just that. stay tuned.

Further reading:

Inflation matters more than interest rates to the stock market