sponsored by

As we emerge out of the pandemic, we do so in light of the experiences of the past two years, deeply changing. Capital markets are no different. They, too, are quite different from what started in January of 2020. At the height of the pandemic-induced selloff in March 2020, we saw rapid volatility, and while the sell-off and subsequent rebound was extremely sharp, it marked a transition into a more volatile market that we are still experiencing today- Even though the world slowly returns to the (new) normal. The following analysis examines this seismic shift and makes the case for the ongoing need to hedge against market uncertainty resulting from more frequent and higher spikes in equity volatility.

then and now, higher and more frequent volatility

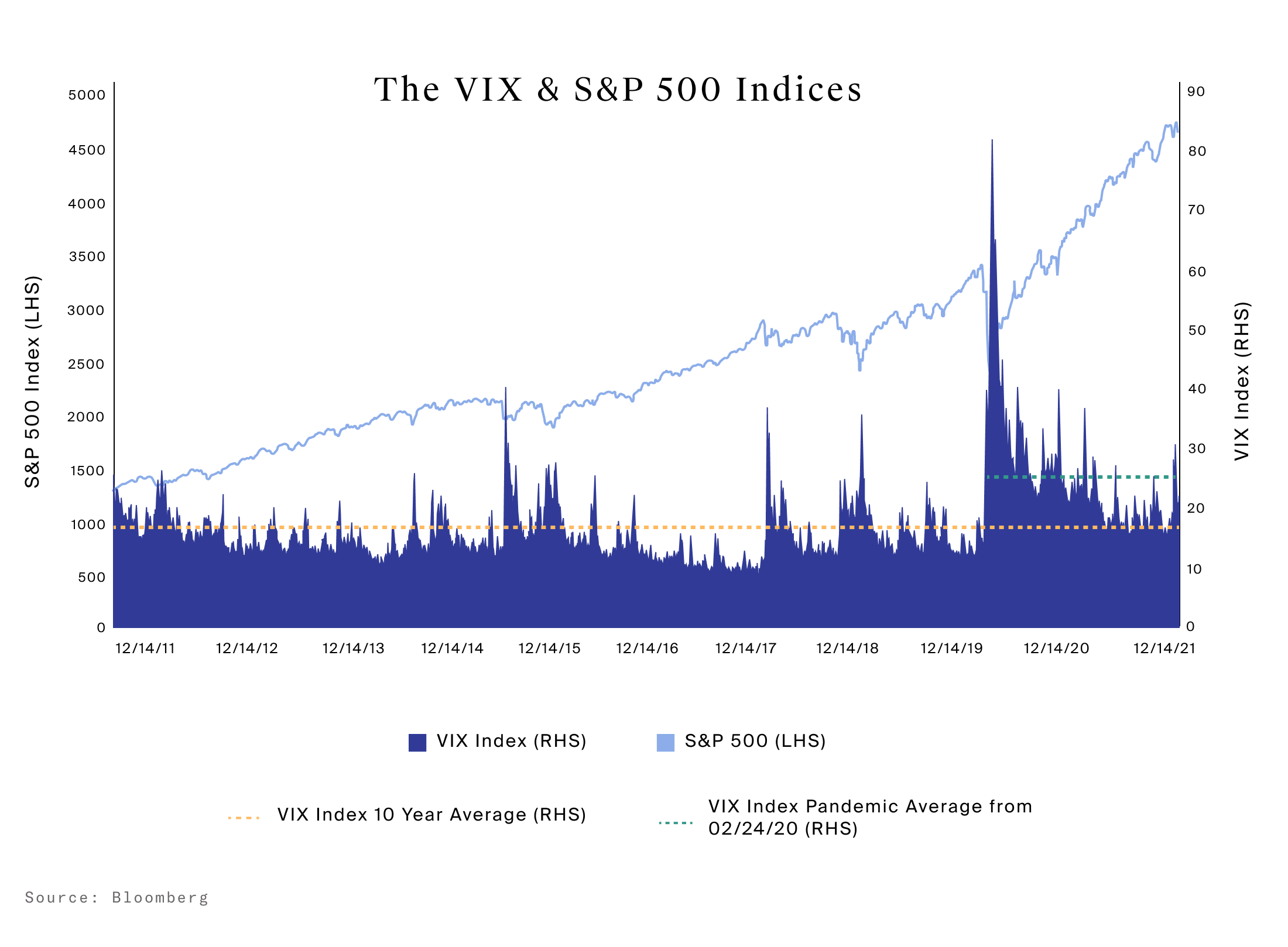

Historically, after periods of extreme and prolonged volatility it is typical for investors to ‘feel’ as if markets have returned to normal levels relatively quickly, with more recent emphasis on low relative volatility, Exhibiting a General Recency Bias[1], However, it takes enough time for the unpredictable atmosphere to dissipate and return to stability. To illustrate this, we can look at the CBOE VIX Index over the past 10 years which displays general expectations for future volatility. During this period, the VIX index averaged a level of 17.1 which compares favorably to the true real volatility of the S&P 500 index, which had a standard deviation of 16.4% over the same period. If we zoom in to focus on the point at which the VIX moved through its 10-year average on February 24, 2020 to the present, the VIX pandemic period average jumps to the level of 25.4 and The actual volatility more than doubled to 27.0%. While the VIX has been running lower lately, volatility has a long runway before it returns to normal. This implies that investors should expect higher volatility in the near term.

Apart from experiencing a volatile equity environment, we are also experiencing more frequent and higher spikes in the VIX Index. Seven of the 10 biggest spikes in VIX over a 10-year period occurred during the current pandemic. The frequency between spikes in the VIX has also accelerated significantly, lasting 589 days and reaching an average peak index level of 38.0 before the pandemic, which now occurs every 75 days and an average peak index of 43.1. level is reached. At the peak of the pandemic, the S&P 500 dropped -33.9% in just 24 days. It then took 104 days (4x duration) to recover on August 18, 2020. More frequent and higher spikes in volatility, as we are currently experiencing, have the potential to significantly affect an investor’s ability to build wealth, adding further uncertainty. How long will it take to do this? Thus, it may be prudent for investors to consider flexible, short dated hedging strategies that can adapt to the dynamic nature of the broader market volatility environment.

For example, we have seen financial advisors guide their clients to invest in defined outcome strategies, such as structured notes that can provide downside protection through buffers and barriers, a potential hedge against this type of volatility. can act as Additionally, we have seen strong demand for equity hedge and multi-strategy hedge funds given their ability to offer non-correlated returns within a tightly controlled risk framework.

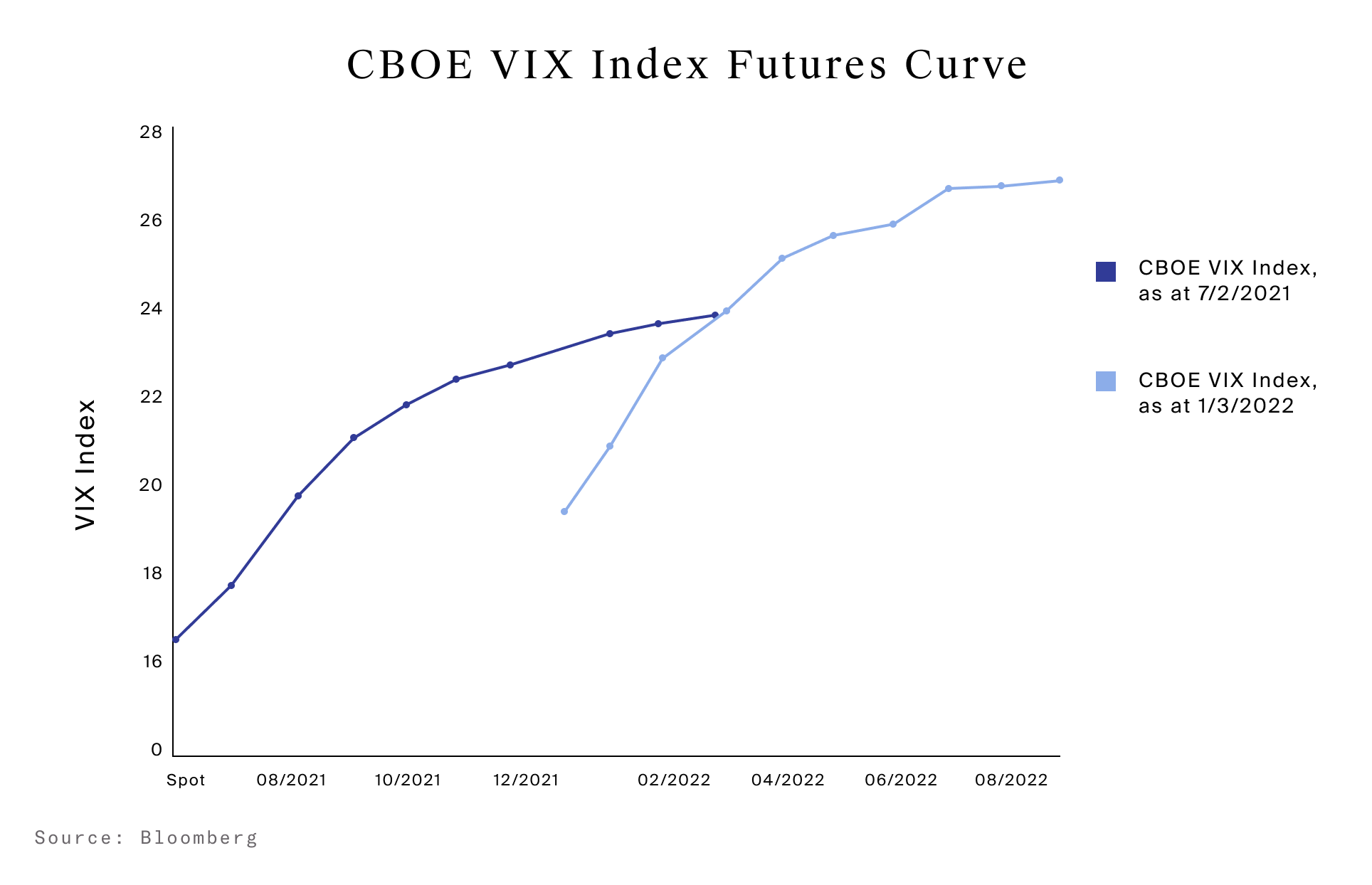

Finally, recently we have noticed a significant shift in the VIX Index futures curve. Over the past few months, the futures curve has shifted higher, indicating that expectations are rising for volatility in the US equity market over the next several months. The move was also accentuated in the backwardness of the curve for the 6 days ending December 3, 2021, essentially reflecting extreme current volatility, while it is expected to remain high in the future as well. Bloomberg noted that the last time this happened was in January, when the same-stock fuel rally ended. It tracks current expectations for future volatility in US equities via the VIX Futures Curve, confirming a continuation of the trend towards higher and more frequent spikes in volatility – a trend we have seen since the pandemic began Is.

In short, we believe the current volatile market is here to stay as we work through a possible end to the pandemic, and monetary and fiscal policy returns to normal. In such an environment, financial advisors are best served by managing their clients’ portfolios through this lens.

1. Morningstar, “Is Recency Bias Influencing Your Investment Decisions?”, April 27, 2020, https://www.morningstar.com/articles/979322/is-recency-bias-swaying-your-investing- decisions