Long Term Financial Goals to Secure Your Financial FutureLong-Term Financial Goals: How To Plan Your Financial Future at Any Age

Long-term financial goals take five or more years to accomplish and generally apply to major life events. Some of the most important long term financial goals people have include saving for retirement and paying off their mortgage.

It’s natural to feel overwhelmed when thinking about your finances several years down the road. Seeing your responsibility for a mortgage, credit card debt, or personal loan can often feel unmanageable when viewed as a whole. The key to overcoming this feeling is to prepare yourself long before the need arises. Setting long-term financial goals early in life can make the process more manageable.

Long-term financial goals take five or more years to accomplish and generally apply to major life events. To boot: You can set them anytime in your life. This guide breaks down how to set a long-term financial goal at any stage of your life and provides tangible financial goal examples to inspire your planning.

Why Are Long-Term Financial Goals Important?

If you only focus on financial goals relevant to your current situation, you may find yourself unprepared when you experience future life events. For example, saving an emergency fund is an incredibly useful short-term goal, but if you don’t save money outside of that fund, then you will be unprepared for retirement. Long-term financial goals bring awareness to events that may be decades away and help to ensure you’ll be prepared for when they arrive.

Long-Term vs Short-Term Financial Goals

While long-term financial goals focus on several years into the future, short-term goals are concerned with the present. Short-term goals can generally be accomplished within a year and are usually easy to achieve. Typical short-term financial goals include establishing a monthly budget and saving an emergency fund. Establishing key short-term goals can help investors achieve their long-term money goals by getting them on the right track early on.

Long-Term vs Mid-Term Financial Goals

Mid-term financial goals are a gray area in financial planning. They often overlap with short and long-term goals—taking longer to achieve than short-term goals, while less difficult than long-term goals. Saving for a down payment can fall under either type of financial goal since the amount you need to save can vary based on the size of the purchase. It can take more than five years to save up for a house down payment depending on your income and the cost of the house.

Long-Term Financial Goals For Your 20s

Your 20s represent a unique time in your financial journey since many people start out with a blank page. Knowing where to begin can be a challenge, but this time in your life has the power to set the stage for decades to come. Setting financial goals now can improve your quality of life and answer the question, “Where should I be financially at 25?”

Identify Your Retirement Needs

Although your retirement is likely several decades away, identifying your future needs will increase your likelihood of meeting them when they arise.

Think about likely expenses you’ll have at this time in your life. How much might you receive from social security? Will you have rent or mortgage payments? How much will you need to receive from your retirement account to cover your estimated retirement budget?

You can build your current monthly savings plan around your expected future needs. Comparing these needs to your current income will help you determine if these goals are realistic and if you need to find new income streams.

Open a Retirement Account

Saving money early on is the one of the greatest ways to secure your financial future. The interest you earn on your savings will compound, leading to exponential growth by the time you’re ready to withdraw it. The rule of thumb is to save 15 percent of your pre-tax income each year.

There are multiple options for where to invest your money. A couple of the most common include individual retirement accounts(IRA) and 401(k)s. It can be very beneficial to participate in your employer’s retirement program since they often include company contributions, which is like an addition to your salary.

Save For a House Down Payment

Most people dream of owning property. Building equity in an appreciating asset instead of spending money on rent can be a great way to eliminate future expenses after you pay off the mortgage.

The amount of money you need to save will be dependent upon the cost of your desired home. A down payment of 20 percent can lower your interest rate and eliminate the need for private mortgage insurance (PMI). If your desired first home costs $300,000, then you will need a down payment of $60,000 to meet this requirement. Smaller down payments are possible, but they will affect your interest rate and the likelihood of being approved for the loan.

Pay Off Credit Card Debt

Credit cards can allow you quick access to funds when you need them most, but carrying credit card debt can quickly wipe out your financial progress. In a perfect world, you’ll be paying off your credit card monthly without accruing any interest.

In the event that you have accumulated credit card debt, it should be a top priority to pay it off. High interest rates, sometimes surpassing 15 percent, offset the gains you’d be making by investing that same money while holding the debt. Use a credit card payoff calculator to learn how long it will take to settle your debt.

Increase Your Earnings Potential

Making more money is the simple answer to securing your financial future, but how do you go about making it happen? Evaluating where you want to be in five years is a great starting point. Does your career path require a higher level of education than you currently have? Does your current job have a glass ceiling preventing growth?

Talk to your boss about your aspirations. There may be training they can recommend to put you on the ladder of success. If your current employer is unable or unwilling to help, consider upskilling on your own. Get certifications independently or enter a graduate program. Proactively finding ways to increase your earnings is better than wasting years at a dead-end job.

Long-Term Financial Goals For Your 30s

Entering your 30s often brings a new degree of stability to your finances. Ideally, you will be on a career path that allows you to meet most of the long-term financial goals you set for yourself in your 20s. However, with age comes life changes that may require you to shift your priorities.

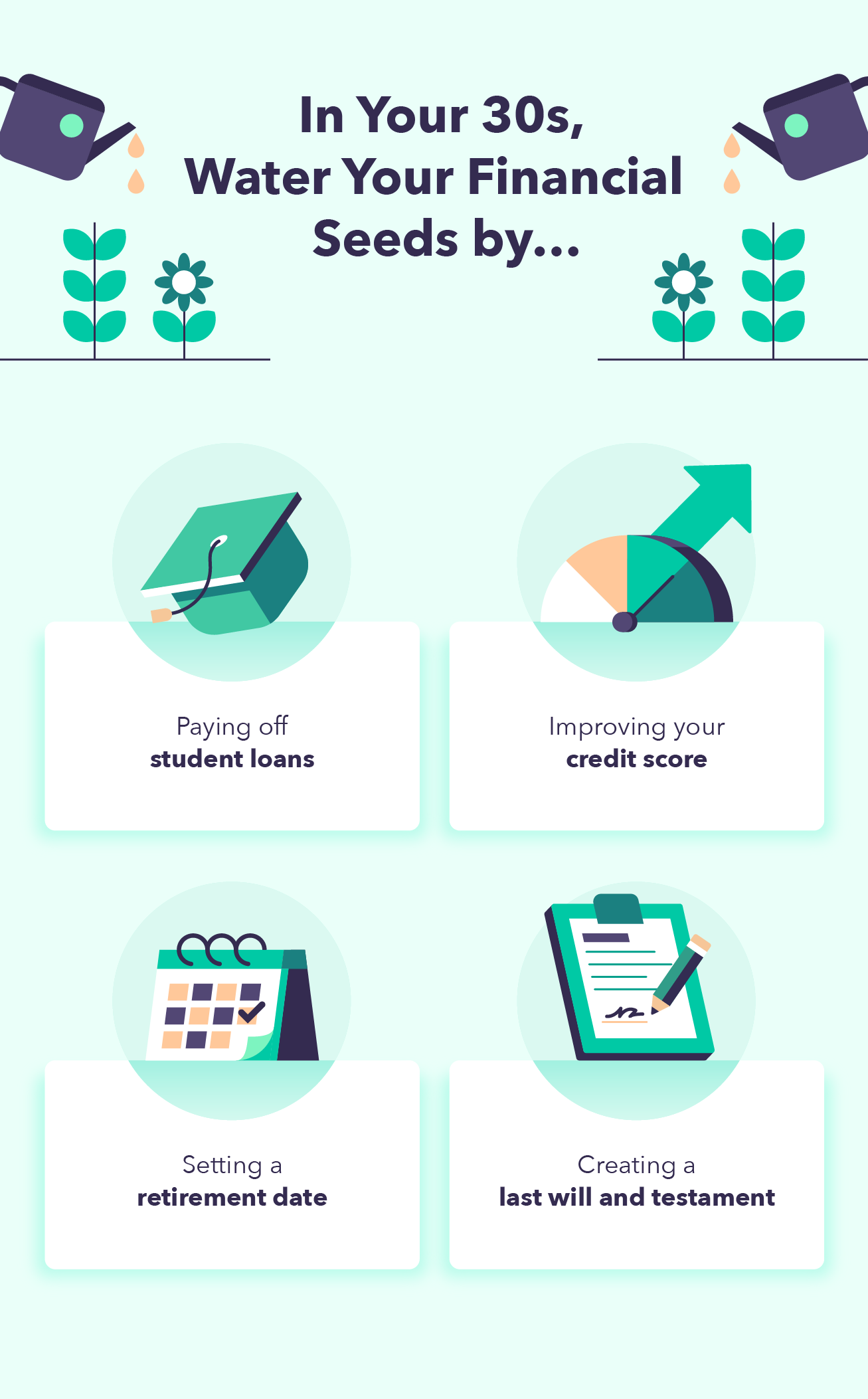

Pay Off Student Loans

The sooner you pay off your debts, the more money you can put toward other financial goals. If you have no higher commitments, it can be better to aggressively pay off your student loans early. Variable loans may be manageable for you at the moment, but if interest rates rise, your loan could quickly increase by more than 5 percent.

Large payments are not a possibility for every investor’s goals. Putting just 10 percent of your gross income toward your student loans can still be enough to whittle away your outstanding debt. As your income increases, aim to pay a larger monthly amount until the loan is eliminated. Using a student loan calculator can help make your goal attainable.

Improve Your Credit Score

A good credit score makes it easier to meet a number of personal financial goals. You can get approved for a better apartment or receive a better interest rate on your car loan and mortgage payments. Although it depends on the scoring system, aiming for a credit score above 700 will generally give you more favorable terms.

Ways to improve your credit score include:

- Paying your rent on time and not breaking the lease early

- Using 30 percent (or less) of your total credit limit

- Paying your credit cards in full each month

- Keeping old lines of credit open

- Limiting the number of hard inquiries into your credit

- Settling any delinquencies

Set a Retirement Date

In your 20s, you might have had a general idea of when you wanted to retire. In your 30s, it’s time to think about a precise date that you can plan around. Your potential retirement year will vary based on your income, debts, and personal commitments.

If you were unable to stick to the goals you made in your 20s, then you may need to adjust your financial planning for retirement to something more attainable. If you are committed to retiring in a specific year, you may need to ramp up your savings and cut unnecessary purchases. Identifying when your mortgage will be paid off and when your kids will be finished with school can also affect your retirement date.

Create a Last Will and Testament

A last will and testament is the legal document used to allocate your property after you die. It also identifies the executor of your estate—the person responsible for settling your outstanding debts and seeing that your will is honored.

Without a will, your assets will be distributed by the government after you die. This can be a costly process with no guarantee that your wishes will be honored. If you have plans for who inherits your belongings, meeting with an estate planning attorney should be made a priority.

Long-Term Financial Goals For Your 40s

Life in your 40s is full of responsibilities. You likely own more assets now than at any other time in your life, your family is growing, and your goals are changing. Now it’s time to reorient your long-term financial goals to your current situation.

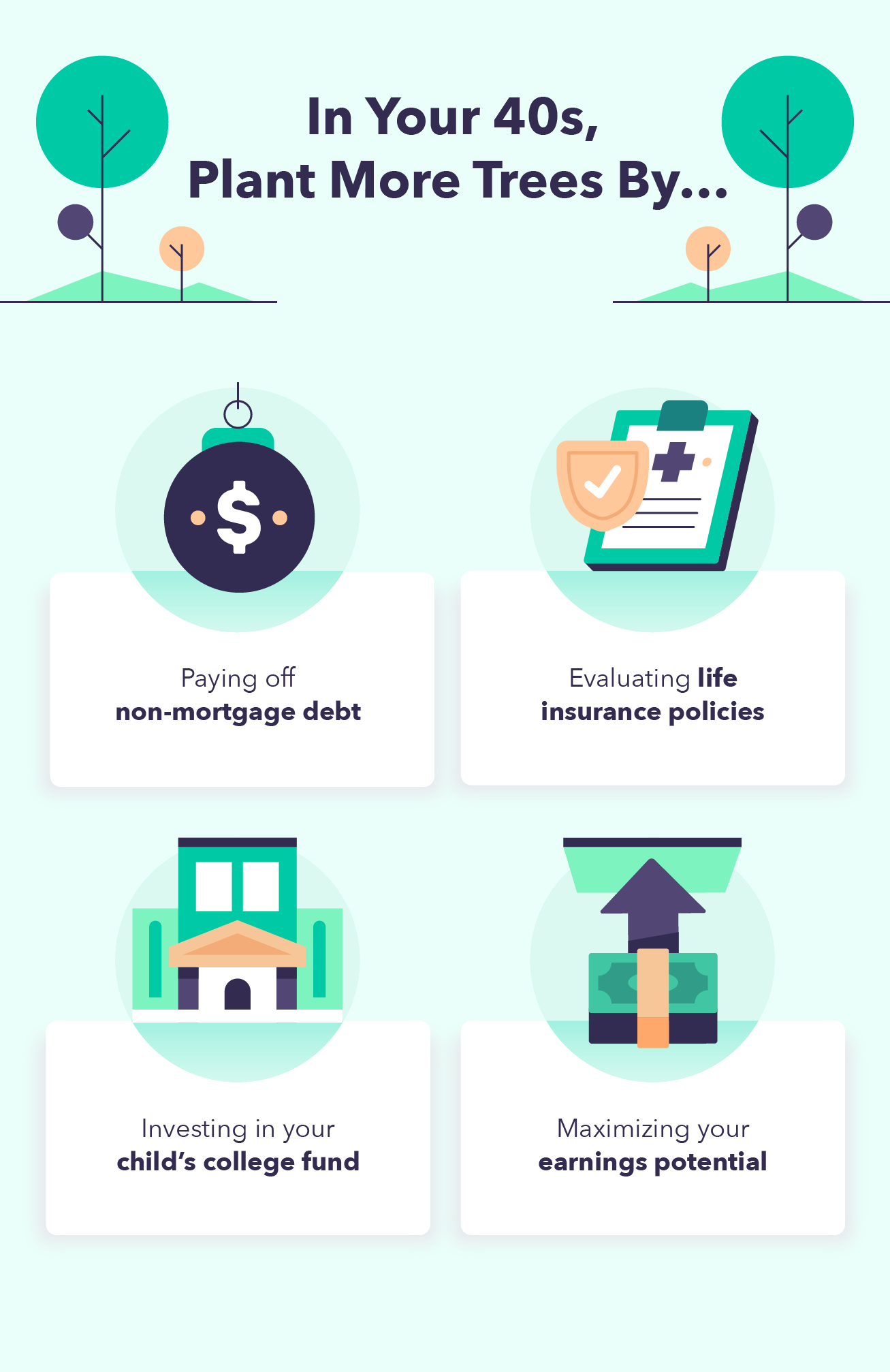

Pay Off Non-Mortgage Debt

Aside from your mortgage, which can follow you into your 50s and 60s, all other debt elimination should be prioritized. Just because you eliminated some debts in your 20s and 30s does not mean new debts haven’t appeared.

You may have new credit card debt or student loans from returning to school. Automobile purchases can happen at any point in life. Regardless of the reason for the debt, you won’t want high APR payments lingering when you are approaching retirement age.

Evaluate Life Insurance Policies

Life insurance is what your dependents will use to bolster their lifestyle in the event of your death. Having a comprehensive policy can ensure their needs are met even if your savings at that time are not enough.

Due to the financial obligations the average 40-year-old has, it is often recommended to purchase more life insurance than you initially thought you’d need. You’ll want to make sure your family can cover their living expenses and settle any debts without your income.

Invest in Your Child’s College Fund

Saving for your children’s education is one of the best ways to set them up for financial success. If they can avoid the early debt of student loans, then they can focus on other financial goals earlier.

A college fund is a large investment and it will take a long time to accomplish. Depending on when you have kids, you may want to start their college fund before your 40s to ensure it is adequate by the time they graduate high school.

Maximize Your Earnings Potential

Most people reach their peak earning potential at some point in their 40s. Putting yourself in a position to maximize this number will set the stage for your quality of life in retirement. A larger income will enable you to max out your retirement contributions.

This is another time to analyze if your current job aligns with your long-term financial plans or if you need to make a change. Look for ways to make more money by negotiating for a raise, earning a promotion, starting a side hustle, or changing employers.

Long-Term Financial Goals For Your 50s and 60s

These two decades in a person’s life often have a large degree of overlap. Your personal commitments are simplified, and your set retirement date is finally within view. All that is left for you to do is tie up loose ends.

Become Entirely Debt-Free

Paying off your mortgage is a major financial goal and getting it done before you retire is a huge accomplishment. Knocking it out while you’re still working full-time enables you to put more money into your retirement portfolio. The same goes for any other outstanding debts that are persisting. These monthly expenses can prolong your time in the workforce past what you originally intended.

Plan Long-Term Care Options

There may come a time in your life when you are no longer able to take care of yourself. You’ll want a plan in place before that happens so your finances will be enough to meet your needs. Make sure your family is aware of your wishes so they can prepare as well. Some things to consider include:

- Who will be your guardian?

- Will you receive in-home care or move to a live-in facility?

- If you require a live-in facility, which one will it be?

Long-term care services are a costly addition to your retirement budget. Setting up funding for such an event years before the need arises can make it more manageable.

Re-evaluate Your Estate

Many changes may have occurred in your life since you first drafted your will. Re-evaluating what assets are currently in your possession will make the process of managing your estate go much smoother. This is another opportunity to discuss your financial affairs and wishes with your family. Avoid unexpected revelations after your death, so there isn’t fighting amongst your loved ones.

Downsize Your Living Expenses

Implementing cost-cutting measures in your life before retirement can help put your future lifestyle into perspective. You may realize that your initial retirement budget can’t meet your needs and you need more time to save.

The house you raised a family in may no longer be necessary once your kids are out of the house. Selling it for a smaller property can add to your savings while reducing expenses. The same can be said for owning multiple vehicles or vacation properties.

Everyone has unique needs and obligations that influence their financial journey. Budgeting and saving can keep you on track to meet your long-term financial goals. Regardless of where your finances stand today, it’s always a great time to prepare for many of life’s important events.