cost of goods sold definition

Cost of goods sold (COGS) is the cost of producing goods sold by a company. It directly accounts for the cost of materials and labor related to that item and for a specified accounting period.

As a company that sells products, you need to know the costs of making those products. That’s where the Cost of Goods Sold (COGS) formula comes in. In addition to calculating the costs to produce a good, if price changes are necessary, or you need to deduct production costs, the COGS formula can disclose profits for an accounting period.

Whether you prefer yourself as a business owner or a consumer or both, understanding how to calculate cost of goods sold can help you learn more about the products you buy. Are – or are producing.

What is the cost of goods sold?

Cost of goods sold is the cost of producing the goods sold by a company. This includes the cost of materials and labor directly related to that item. However, it does not include indirect expenses such as cost of distribution and sales force.

What is the Cost of Goods Sold Formula?

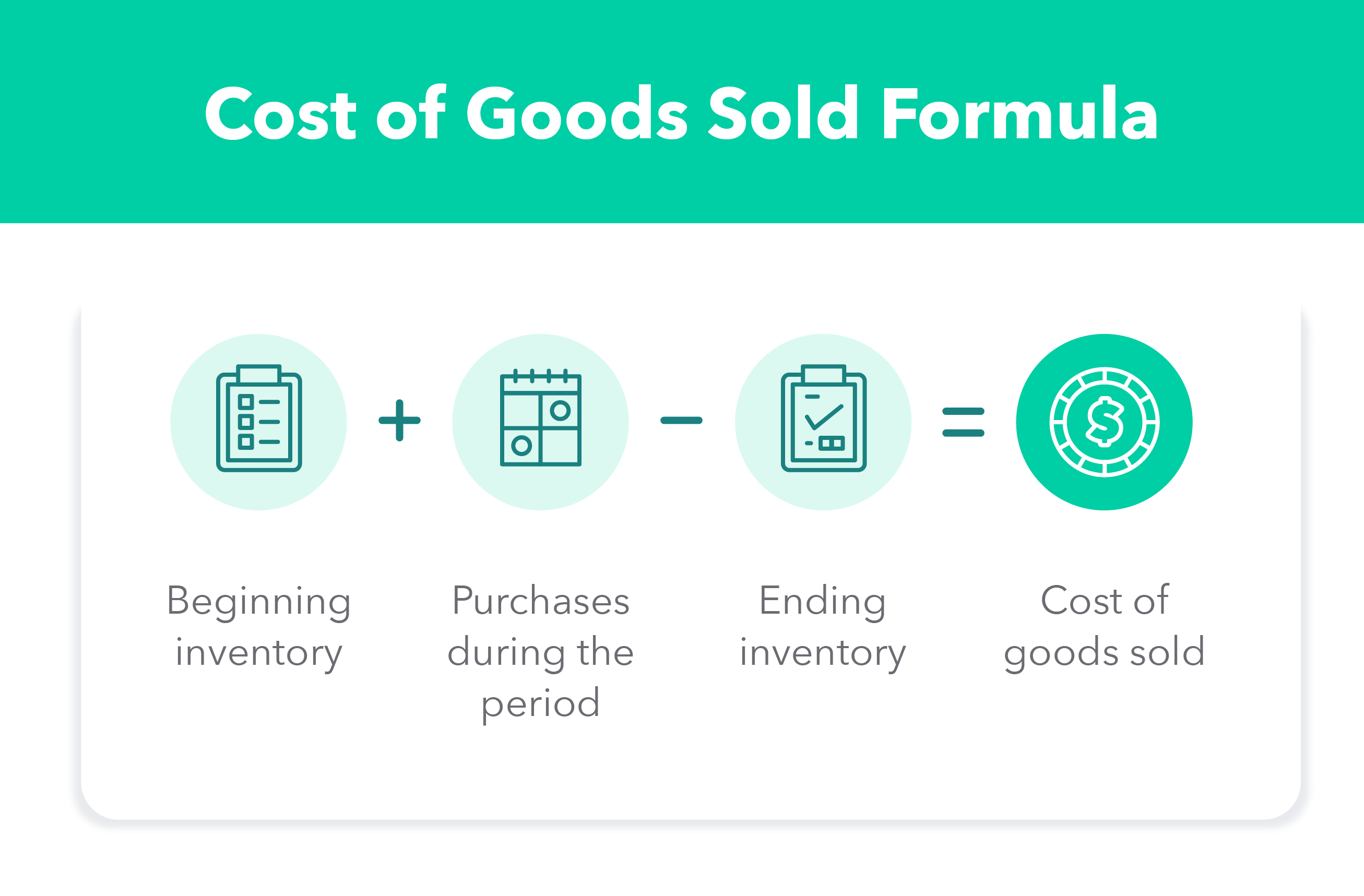

When selling a product, you need to understand the production costs associated with it over a given period, which could be a month, quarter or year. You can do this by using the cost of goods sold formula. This is a straightforward calculation that accounts for beginning and ending inventory, and purchases during the accounting period. Here’s a simple formula for cost of goods sold:

| COGS = Opening Inventory + Purchases During the Period – End Inventory |

How do you calculate cost of goods sold?

To calculate cost of goods sold, you need to determine your opening inventory — meaning your inventory, including raw materials and supplies, for example — at the beginning of your accounting period. Then add in the new inventory purchased during that period and subtract the final inventory — which means the remaining inventory at the end of your accounting period. The expanded COGS formula also includes returns, allowances, exemptions and freight charges, but we stick to the basics in this explanation.

Taking it one step at a time can help you understand the COGS formula and find the true value behind the item being sold. Here is how you do it:

Step 1: Identify direct and indirect costs

Whether you manufacture or resell products, the COGS formula allows you to deduct all costs associated with them. The first step is to separate direct costs, which are included in the COGS calculation, from indirect costs, which are not.

direct cost

Direct costs are the costs associated with the production or purchase of a product. These costs can fluctuate depending on the production level. Here are some direct cost examples:

- direct labour

- direct materials

- manufacturing supplies

- fuel consumption

- power consumption

- production staff wages

indirect costs

Indirect costs go beyond the costs associated with producing the product. These include the costs involved in maintaining and running the company. There may be fixed indirect costs, such as rent, and fluctuating costs, such as electricity. Indirect costs are not included in the COGS calculation. Here are some examples:

- utilities

- marketing campaign

- office supplies

- Accounting & Payroll Services

- insurance cost

- Employee Benefits and Perks

Step 2: Set the Preliminary List

Now is the time to determine your starting list. Opening inventory will be the amount of inventory left over from the previous time period, which could be a month, quarter, or year. Starting inventory is your inventory, which includes raw materials, supplies, and finished and unfinished products that were not sold in the previous period.

Keep in mind that your opening inventory cost for that time period should be exactly the same as the ending inventory for the previous period.

Step 3: Match the items you added to your list

After determining your initial inventory, you’ll also need to account for any inventory purchases throughout the period. It is important to keep track of the cost of shipment and manufacturing for each product, which adds to the inventory cost during this period.

Step 4: Set the Expiration List

Final inventory is the cost of goods left over in the current period. This can be determined by taking a physical inventory of the products or by estimating the amount. If an inventory is damaged, obsolete or worthless, the final inventory cost can also be reduced.

Step 5: Plug this into the cost of goods sold equation

Now that you have all the information to calculate cost of goods sold, all that’s left to do is plug it into the COGS formula.

An Example Formula of Cost of Goods Sold

Let’s say you want to calculate cost of goods sold over a monthly period. After accounting for direct costs, you find that you have an initial inventory of $30,000. Throughout the month, you buy an additional $5,000 worth of inventory. Finally, after taking inventory of the products you have at the end of the month, you find that there is a final inventory worth $2,000.

Using the cost of goods sold equation, you can plug those numbers in and find that your cost of goods sold is $33,000:

| COGS = Opening Inventory + Purchases During the Period – End Inventory |

| COGS = $30,000 + $5,000 – $2,000 |

accounting for cost of goods sold

Various accounting methods are used to record the level of inventory during the accounting period. The accounting method chosen can affect the value of cost of goods sold. The three main methods of accounting for cost of goods sold are FIFO, LIFO, and the average cost method.

FIFO: First in, first out

The first in, first out method, also known as FIFO, is when goods purchased first are sold first. Since the prices of traded goods tend to rise, using the FIFO method, the company will be selling the least expensive item first. This translates into less COGS as compared to the LIFO method. In this case, net income will increase over time.

LIFO: Last in, first out

The last in, first out method, also known as LIFO, occurs when the most recent item added to inventory is sold first. If prices rise, a company using the LIFO method will essentially be selling the goods at the highest cost first. This leads to higher COGS as compared to FIFO method. Using this method, net income decreases over time.

average cost method

The average cost method is when a company uses the average price of all goods in stock to calculate beginning and ending inventory costs. This means that the impact of a higher cost in COGS will be less when purchasing inventory.

Considerations for cost of goods sold

When calculating cost of goods sold, there are a few other factors to consider.

COGS Vs. operating expenses

Business owners are likely familiar with the term “operating expenses.” However, it should not be confused with cost of goods sold. Although they are both company expenses, operating expenses are not directly tied to the production of goods.

Operating expenses are indirect costs that keep a company running and can include rent, equipment, insurance, salaries, marketing and office supplies.

COGS and Inventory

The COGS calculation focuses on your business’s inventory. Inventory can be purchased or self-manufactured items, which is why manufacturing costs are sometimes included in the direct costs associated with your COGS.

Revenue vs. Cost

Another thing to consider when calculating COGS is that it is not the same thing as cost of revenue. Cost of revenue takes into account some indirect costs associated with sales, such as marketing and distribution, while COGS does not take into account any indirect costs.

Exclusion from COGS Deduction

Since service companies do not have inventory to sell and COGS accounts for the cost of inventory, they cannot use COGS because they do not sell a product – they will calculate the cost of services instead. Examples of service companies are accounting firms, law offices, consultants and real estate appraisers.

Bottom-line

Running a business requires many moving parts. To ensure that a company is making a profit and everyone is paid a fair salary, business owners must consider the costs associated with goods sold thoroughly. Following this step-by-step guide to learn how to use cost of goods sold is a good starting point. As always, it’s important to consult with an expert, such as an accountant, when performing these calculations to make sure everything is accounted for.

Source: QuickBooks