History doesn’t repeat, but it often rhymes.

I don’t know if it was Einstein, Twain, Munger or someone on Instagram who originally said this, but it’s definitely something people say all the time.

We humans are pattern-seeking creatures so it makes sense that we would constantly look to the past to help explain the present or future.

Recognizing that we are actually going to happen based on what has already happened helps to calm our minds, even though we all know that the future is impossible to predict.

I believe that human nature is a constant when it comes to understanding the markets over time, but I also believe that humans are unpredictable.

while the markets are Always They were different now than they were in the past because our knowledge of past compounds over time, you cannot ignore the fact that some markets feel roughly the same over time.

The current environment of a correction in the overall stock market, while some segments of the market are getting completely slaughtered, has been taunting me for weeks like an actor in a movie that I just can’t keep up with.1

Why does this market sound so familiar when I’ve read in the past?

And then it hits me.

Oh yeah, it’s basically the end of the 1960s go-go years!

Obviously I didn’t live through the go-go years of the 1960s or so but the best book I’ve read about that period is, go-go years, Unique by John Brooks.

The go-go years were a period defined by growth stock outperformance, millions of new retail investors, hundreds of speculators, and star portfolio managers making money based on exceptional performance numbers.

Known?

When things finally fell the overall stock market went into a nasty bear market, down 36%, but the hottest stocks were drilled more like 80%. Brooks explains:

From the peak of September 1929 to the nadir of the Great Depression in the summer of 1932, the Dow industrial average fell from 381 to 36, or just over 90 percent. From the December 1968 peak to the May 1970 low, the same index fell from 985 to 631, or about 36 percent. By that standard, a pistol fired against a mortar barrage. But, as we’ve had the opportunity to note earlier, that standard won’t really hold up; The Dow accurately reflected the market of 1929–1932 when house painters and office girls were taking their plunge into Dow stocks such as General Motors and Standard Oil of New Jersey, and miserably failed to reflect the 1969–1970 market. when the likelihood of a similar decline was far greater. Control must be built into the data or gender-temco-vote.

A financial advisor named Max Shapiro, writing in the January 1971 issue of Dunn’s Review, tried to create a new scale more suited to the new situation. as a rough modern counterpart which was represented by Dow In the old days, Shapiro made a list of thirty major glamorous stocks of the nineteen sixties – ten major conglomerates including Lytton, Gulf and Western, and Ling-Temco-Watt, ten computer stocks including IBM, Lisco, and Sperry Rand, and Ten technology stocks including Polaroid, Xerox and Fairchild cameras. Shapiro found that the average decline from 1969–1970 across ten groups was 86 percent; of computer stocks, 80 percent; of technology stocks, 77 percent. All thirty stocks in this handcrafted Neo-Dow had an average decline of 81 per cent. Even allowing for the fact that the benefits of hindsight gave Shapiro the opportunity to choose to include particular stocks on his list, which would help prove his point, his analysis strongly suggests. Gives that, as measured by the performance of the stocks in which the novice investor was most likely to take their first dip, the crash of 1969–1970 was comparable to that of 1929 as a whole.

Brooks says that the 1968-1970 bear market actually had an even bigger impact on the investing public than the Great Depression. In 1929 there were only 4-5 million people who invested in stocks in the United States. By 1970, there were over 30 million investors.

As far as historical market crashes, it is never mentioned with the likes of the Great Depression, the 1973-1974 bear market, the 1987 crash, the dot-com bust, or the 2008 crash.

The reason for this appears to be that the overall market performance may have hidden some of the pain in the specific stocks and sectors where many investors had allocated their money.

The crash was worse for most investors than what the market showed, especially when you consider that there were no index funds to invest in at the time.

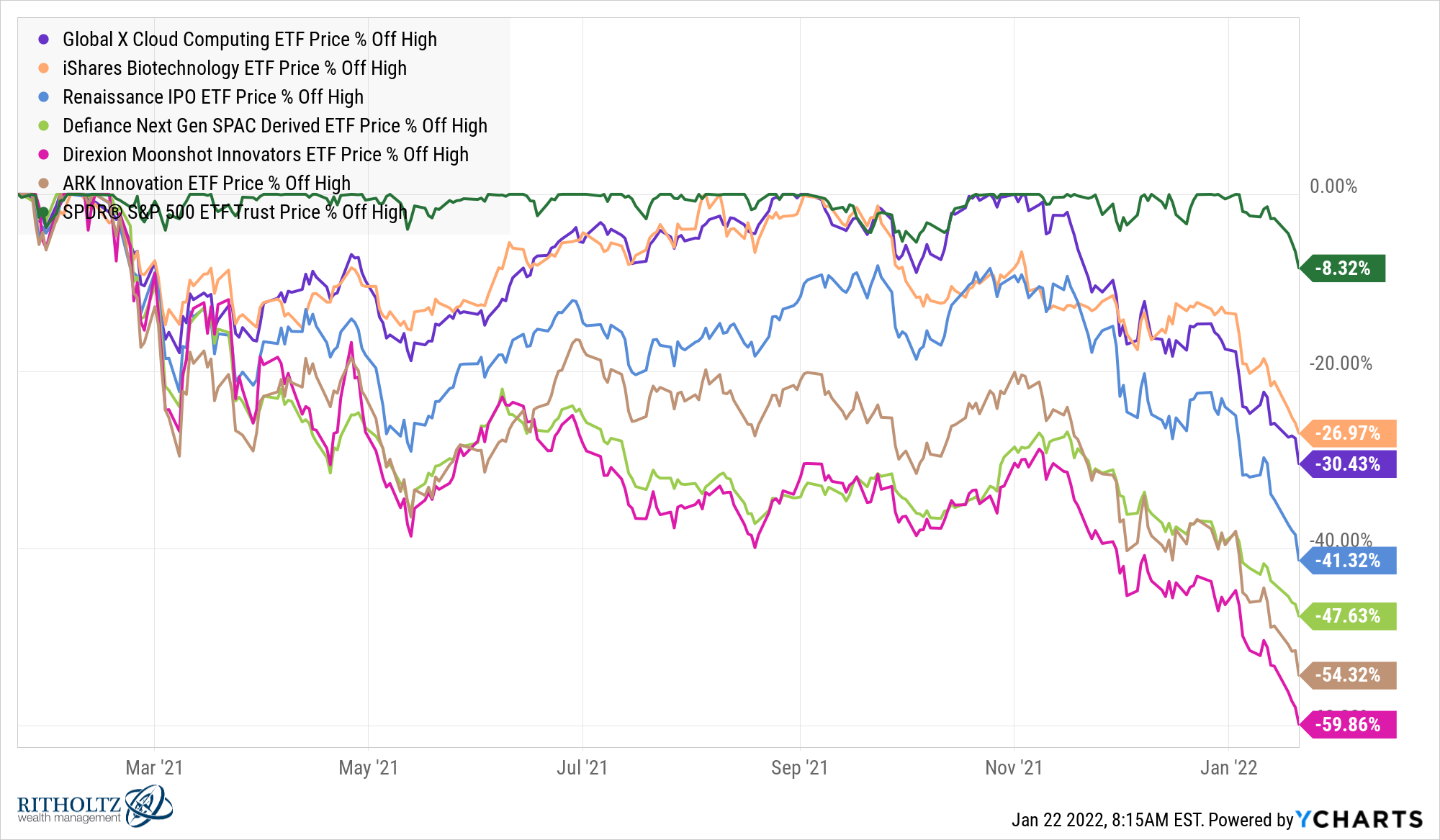

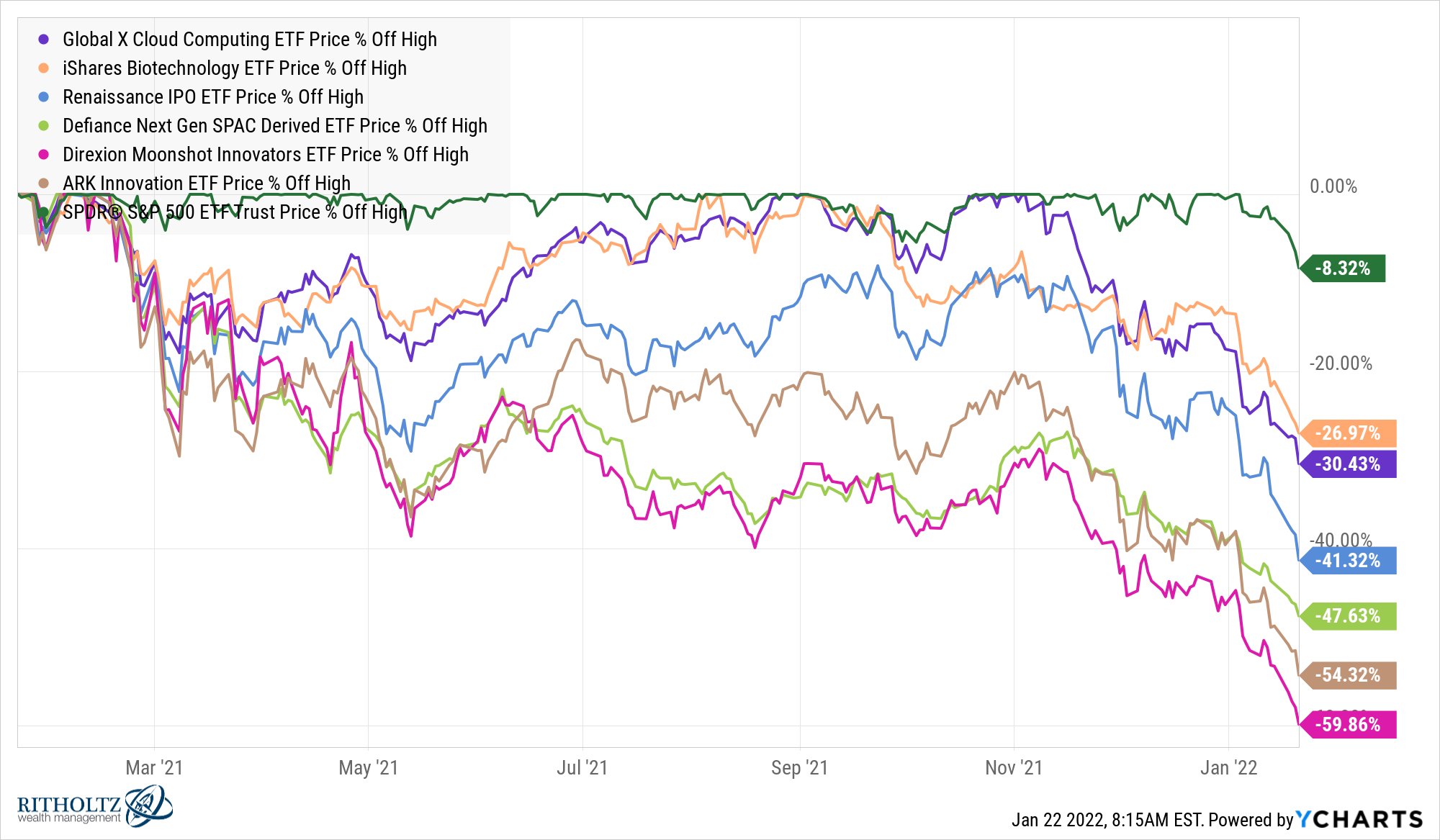

Right now the stock market is not close to a 30%+ bear market, but the gap between the market and the glamorous stocks is as deep as it was then.

Take a look at the current declines on the S&P 500 (-8%) versus losses in cloud computing stocks (-30%), biotech (-27%), new IPOs (-41%), SPAC (-48%). and small (-60%) and large (-54%) innovation companies.

The S&P 500 isn’t even 10% down from an all-time high, while growth stocks are getting wiped out.

And that’s not the only similarity between now and the go-go years.

Here’s what I wrote about Kathy Wood in an excerpt from Jerry Tsai when ARK was on fire:

In Big Mistakes, Michael Batnick profiles Fidelity’s Jerry Tsai, basically the first star fund manager in the 1960s go-go years.

Investors went crazy for mutual funds in general as total fund assets grew from $1 billion in 1946 to more than $35 billion by 1967.

But Tsai stood out from the crowd. After a run of outperformance that began in 1958, Tsai saw the number of shareholders in her fund sextuple from 6k to 36k from 1960 to 1961.

After leaving Fidelity in the mid-1960s to start her own fund, Tsai was crushed in the bear market of 1968-1970, in which momentum stocks died.

Assets fell 90% over the next few years and Tsai’s fund would have the worst 8-year track record of any mutual fund in history.

I’m not ready to nail the Cathy Wood fund’s coffin just yet, but the similarities here are striking.

According to Jason Zweig, the ARK Innovation Fund had just $12 million in assets as of the end of 2016. After a string of astonishing performance numbers, it was just shy of $2 billion by the end of 2018. Then from 2020 to early 2021 after a sequence of impressive performance poured in from the tail end of $13 billion.

Since then the fund has been rigged.

There is never a single reason for the stock market or any particular segment of the stock market to get hit.

It would be crazy to assume that inflation, rising rates and the Fed’s potential rate hikes are not having an effect on growth stocks right now.

But it’s also possible that the biggest reason these stocks are creamy is due to the fact that these companies went crazy and wildly overvalued.

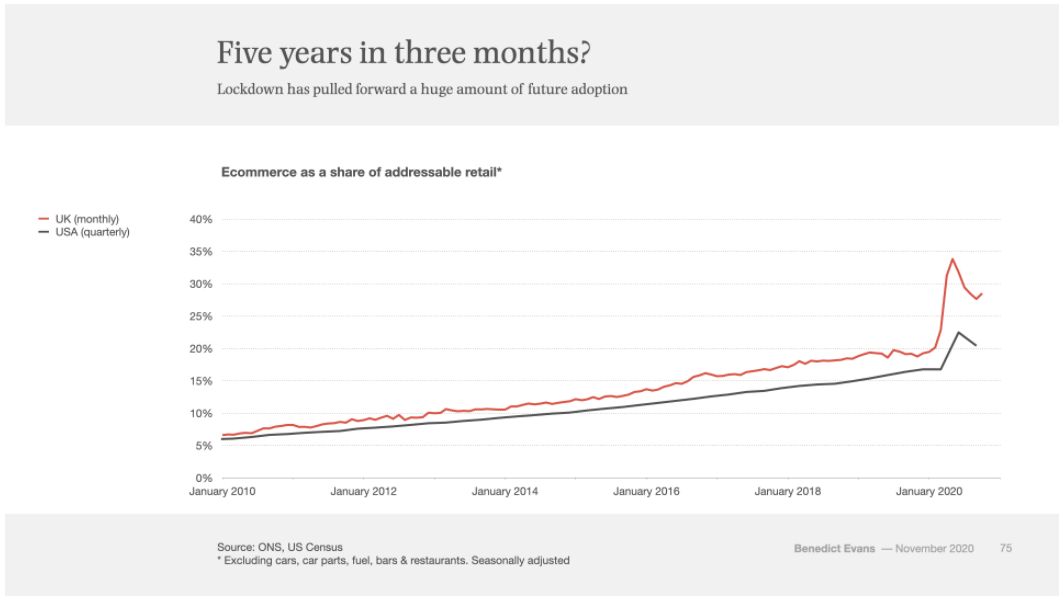

All investors saw charts like this about e-commerce adoption due to the pandemic:

How could you not go in the water after seeing this?

The pendulum always swings very far in both directions, especially when technological innovation is involved. In 2020 and early 2021, that pendulum went very high.

Now that excitement has quickly turned into panic when the mass sales began.

So I don’t want to guess when this current improvement will end.

Will the pain of growth stocks spread to the rest of the market?

Will we see some funds blown up?

Will margin calls create a cascade of sales?

Or is the worst behind us now that the most speculative names have already been crushed?

I don’t know and neither does anyone else.

All I know is that growth stocks were given a long leash to come out of the corona crash.

That’s no longer the case and the go-go years feel like they may be over for a while.

Further reading:

Why the financial frenzy persists

1Thankfully I have IMDb for it.