I wrote the following excerpt before this CNBC story about the Peloton CEO stepping down and laying off 2,800 employees. This was written even before the WSJ story surfaced, about the potential for Amazon to buy the exercise company.

I really think it means a lot to Bezos to buy Peloton. If they roll my Peloton subscription into my Prime subscription it will be fine for me.

But if it weren’t for the pandemic, Peloton probably wouldn’t have been involved in these buyout rumours. I think the pandemic was actually a bad thing for the company’s stock (and a handful of other stocks you might have assumed would benefit from Covid).

This piece I wrote for Fortune explains why.

,

In December 2019, Peloton was an $8 billion market cap company with sales of $1.2 billion and 2 million users.

For an exercise company established in 2012, achieving this size in such a short span of time was quite an achievement. Then the pandemic hit, gyms were closed and millions of workers were introduced to remote work. The company’s development moved to hyperdrive.

By January 2021, Peloton’s customers had grown to 4.4 million, sales had grown to $3 billion, and the stock was trading at a valuation of approximately $50 billion.

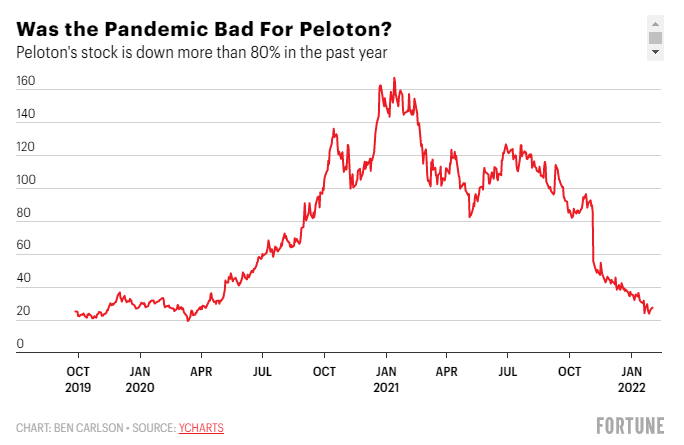

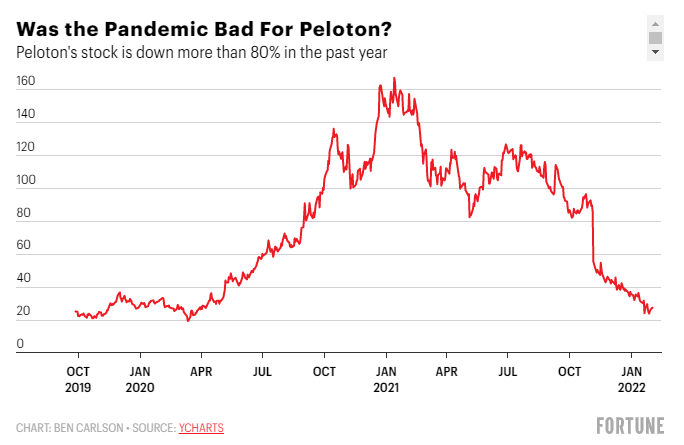

They went from a poor start to one of the most widely known exercise brands in the country. The company now has over $4 billion in sales and 5.9 million users. So the stock must be performing well, right? not enough. This is down more than 80% from last year:

So even though Peloton has more than quadrupled sales and more than tripled the number of users, the market cap is right where it stood at about $8 billion at the end of 2019. The stock price is actually lower now than it was in December 2019, before any increase related to the pandemic occurred.

How can this be?

You could make the case that the pandemic was really the worst thing that could have happened to this company. While the company experienced massive growth in a short period of time, expectations and the stock price rose at an even faster pace. The company couldn’t possibly survive the monster increase in its share price. Peloton’s CEO recently said that the company will have to cut production of its exercise bikes and potentially lay off employees.

Peloton isn’t the only one experiencing an intuitive move in its share price during this strange economic climate.

Netflix had 130 million global subscribers as of the summer of 2018. The share price on the stock was approximately $420/share as of July of that year. At the time the company was turning in an annual profit of about $900 million. With little to do at the start of the pandemic, but with TV watching, Netflix’s subscriber base grew exponentially, reaching more than 222 million homes in 2022. Net income for the company is now $5 billion. Yet the stock price at around $440/share isn’t much higher than it was in 2018. This is down more than 30% from last year’s high.

Like Peloton, Netflix’s growth numbers were great during the pandemic. This set the bar very high for future development. In fact, the company acknowledged as much on its most recent quarterly earnings call. Here’s what CFO Spencer Newman said in a call with analysts:

So overall, business was healthy. Retention was strong. The churn was down. Had to look up. But on the margin, we just — we don’t grow acquisitions as fast as we’d like to see, and on our large customer base, a small change in acquisitions can lead to a huge influx in paid net additions. And then, our acquisitions were growing, just not growing as fast as we were probably expecting or predicting.

The company’s fundamentals have improved over the past four years, but investors’ expectations were even higher than the share price. Hence, the performance of the company’s shares has been weak.

There are other companies that were early beneficiaries of the pandemic that are now facing similar growing pains. Zoom (-73%), Teladoc (-73%) and Robinhood (-79%) all saw strong growth due to the way this pandemic is affecting our lives. Yet their stock prices have plummeted, even as their infrastructure has improved.

One of the hardest parts of investing in stocks comes from the fact that expectations drive almost everything in the short term. Veteran investor Howard Marks puts it this way:

Level 1 thinking says, “This is a good company; Let’s buy the stock.” The second level of thinking says, “It’s a great company, but everyone thinks it’s a great company, and it’s not. So the higher the stock price and the higher the price; Let’s sell.”

Of course, Peloton, Netflix, Zoom, Teladoc, Robinhood or any other growth stock that’s just ending could get its mojo back. The pendulum is always swinging back and forth between optimism and pessimism, enthusiasm and despair.

In the short-run, each stock is some combination of fundamentals, trends, assumptions and stories that investors tell themselves. All these evaluations are in many ways—stories. Stories about growth, potential and what the future might look like for the company.

Unfortunately, investors were bracing themselves for some of the hottest stocks during the pandemic when reality didn’t live up to expectations.

This piece is basically . was published in Luck,