For the second edition of his book, irrational exuberance, Robert Schiller prepared a database of home prices in the United States in 1890.1

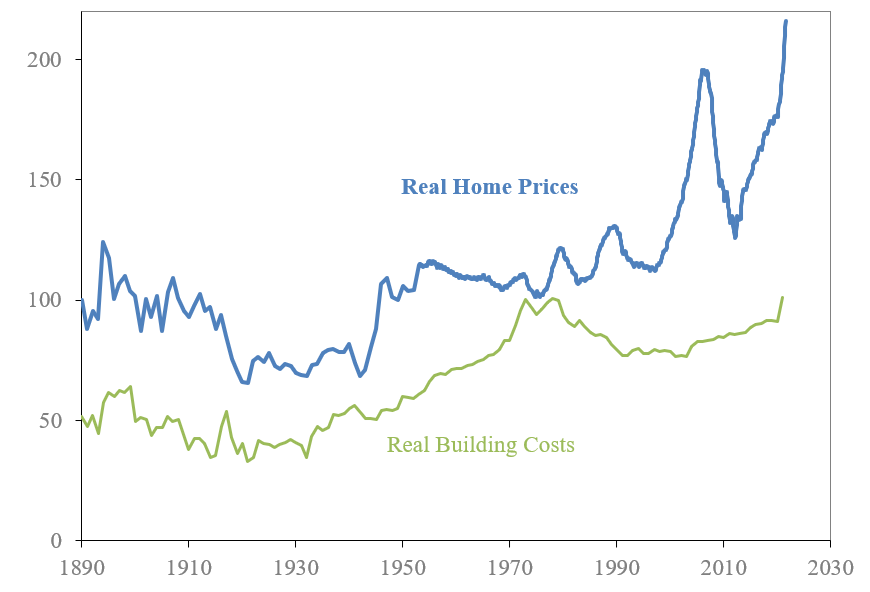

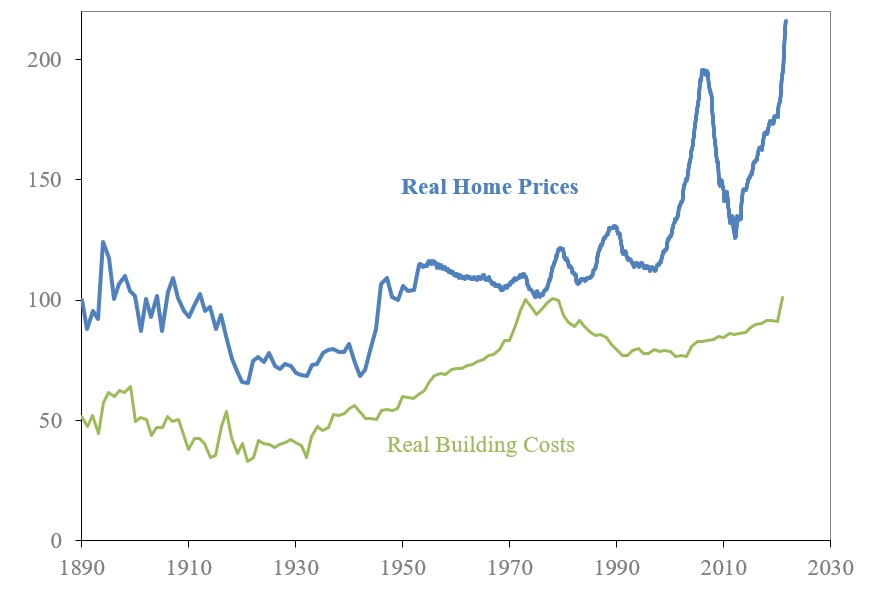

His timing was impeccable. Schiller’s data shows that just as the housing bubble was about to pop, US housing prices were way out of historical data.

It was an excellent call backed by data.

Schiller showed real housing, after adjusting for inflation, returned little to long-term homeowners.

In fact, from 1890 to 1996, Total The actual return for housing in the United States was just 13%. That’s a real annual return of just 0.1% per year for over 100 years.

This was not necessarily a bad thing as housing prices kept up with inflation over the long term. But this will be a disappointing result for most homeowners, especially when compared to other financial assets such as stocks.

Then from 1997 to 2006, real housing prices increased by more than 70%, exceeding the rate of inflation for 10 years at about 6%.

We all know what happened next. The housing bubble burst and prices nationwide fell 35% on a real basis from the bottom in 2012.

Schiller was proved right and it became clear that the American Dream was not as good an investment as it was advertised.

But then a funny thing happened.

The housing route did not work. Prices have recovered those losses and then some:

From down in 2012, housing prices are up more than 70% on a real basis. Prices are much higher than in the bubble of the mid-2000s.

And the crazy thing is that this housing boom bears almost no resemblance to the stories told by Michael Lewis. the big short,

This time the borrowers have better credit profile. Their cost of borrowing is low. They are not taking out risky adjustable mortgages with teaser rates that will be significantly higher in a few years. And this is not a bunch of people who want to flip houses to earn quick money. It is the largest demographic in search of roots.

Is it possible that Schiller was always wrong? Do we all have a recessive bias from the housing crash? Is a home really a very good investment option?

The answer to all three questions is- maybe?

I honestly don’t know how much we can trust housing data going back to the late 1800s. I’m looking at 1883 now and they had a pretty hard time crossing the river without people dying so I’m not sure how good their housing records were.

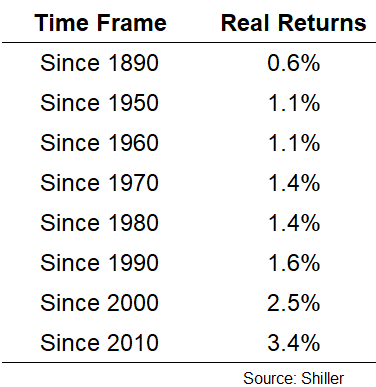

Despite this, there has been an upward trend in real annual returns for US housing over time:

I’m not suggesting that this upward trend will continue and there are certainly some caveats you can make here but modern times are probably more relevant than 19th century figures.

Owning a home wasn’t really known as the American Dream until the 1950s.

World War II had just ended. You prepared all these soldiers to come home to start their lives. The GI Bill helped provide low-cost mortgages but they also needed homes to live in and that was a problem.

Housing was crushed during the Great Depression. Before the Great Depression the United States was building one million homes a year. By the end of WWII this number had fallen to less than 100,000. Housing supply shortage was an all-out crisis.

Yet unlike the situation today, the government at that time actually did something about it. He enacted a comprehensive federal housing bill that gave builders a ton of rebates and guaranteed mortgages. So the builders went crazy.

All over the country they were spitting in houses like an assembly line for the middle class. And they were affordable, at about $5,000 per cookie-cutter house (that’s the average family’s salary for two years’ work).

David Halberstam explains what happened next in his book Fifties:

The accumulated energy of two decades was thrown out. In 1944 only 114,000 new single households were started; By 1946 this figure had risen to 937,000: 1,118,000 in 1948; and 1.7 million in 1950.

The suburbs exploded with about 60 million people moving out of cities from 1950 to 1980. This explosion prompted more people to live in the suburbs than in the cities for the first time.

This building spree lasted well into the 1970s but has been in decline since then. While the country built an average of 15 million new homes per decade from the 1970s to the 2000s, the population is much higher than at that time.

Here’s what I wrote back in May:

In the early 1970s there were about 210 million people in the United States and they were building more than 2 million homes a year. Now there are 33 crore people and last year less than 13 lakh houses were completed.

The combination of rising housing prices and fewer homes to be built has created a situation where a home is probably a better investment option than before.

In many countries outside the United States, the situation is even worse. These statistics from Work in Progress are bananas:

The most dramatic evidence of housing shortages can be seen in the rise in prices over the past forty years. Home prices in the average New York City metropolitan area are up 706% (or 376% higher than US consumer prices, and 326% higher than US wages) since 1980. The increase for San Francisco is 932%. London home prices are more than 2,100% (or about 1500% higher than wages) over that period. In Sydney, Australia prices have increased by 1,450% (compared to an hourly wage increase of 480%). In Ireland, prices have increased by about 800% over that period, driven by growth in Dublin in particular.

I am not suggesting that buying a home is a slam dunk investment. nothing.

There are still issues with housing as a financial asset. Most people underestimate all the ancillary costs involved – property taxes, insurance, maintenance, upkeep, renovations and borrowing costs.

It is also difficult for most people to calculate the actual return because you have to live somewhere. And I’m not sure how Schiller takes into account the implied leverage involved in the equation because most people aren’t buying homes with cash.

Now you can make the case that there is some novelty bias in my position here as well. Prices have been very high over the past decade. Interest rates have fallen. It will be difficult to see this situation repeat itself in the next 10 years.

So maybe where I fall in on this is housing is a cyclical investment opportunity. At times it can be a wonderful investment. Other times it’s just a place where you live, while not necessarily rich.

Michael and I discussed the pros and cons of housing as an investment on this week’s Animal Spirits:

Subscribe to Compound so you never miss an episode.

Further reading:

we need to build more houses

1You can download the data here.