A reader asks:

You guys have been absolutely wonderful in teaching us some valuable lessons. Hate to admit it, I’m absolutely terrible at investing. My ability to withstand down markets is terrible. I don’t want to save cash for the rest of my life, but I also have such a low risk tolerance. Age 31. Goals include getting married/buying a nice house etc. in a strange position. any idea?

It’s the opposite tone of most of the questions I get from young investors these days. For the past few years my inbox and DMs have been filled with youngsters seeking my blessings to invest all their money in crypto, growth stocks or 3x leveraged stock market funds.

It is understandable that given the environment we have been through, young people would want to take more risks. There were tremendous gains in a variety of investments and markets prior to the recent correction.

Also, the threshold of risk is higher among young people these days. I’m not saying this is good or bad, but how the market behaved in your formative years can have a huge impact on your relationship with risk.

Of course, there are many other factors at play that determine risk appetite.

Building the right portfolio requires some balance between your willingness, ability and need to take risk.1 The hard part is sometimes these factors don’t align with each other.

Here our reader is 31 years old. They have great risk appetite when it comes to retirement savings.

Not only do they have 30-40 years till their retirement age, but they also have an additional 20-30 years to invest during retirement. For a 31 year old person the time limit can be 50-70 years.

The combination of a long time horizon and plenty of human capital in the form of future savings from increasing your income makes investing in stocks a no-brainer.

However, sometimes your ability to take risks contradicts your willingness to accept the risk.

Some people just don’t have enough personality to go through the downturn in the stock market. Good thing this reader knows. The worst thing you can do is invest your portfolio using someone else’s willingness to take risks.

To paraphrase George Goodman: The stock market is an expensive place to find out who you are.

Knowing yourself as an investor is a big first step. It takes many investors decades to learn this lesson. never do anything.

But you still have to invest your money in something. You can’t just bury it in your backyard and hope for the best.

Some of the different levers you can consider if you have a low tolerance for risk are:

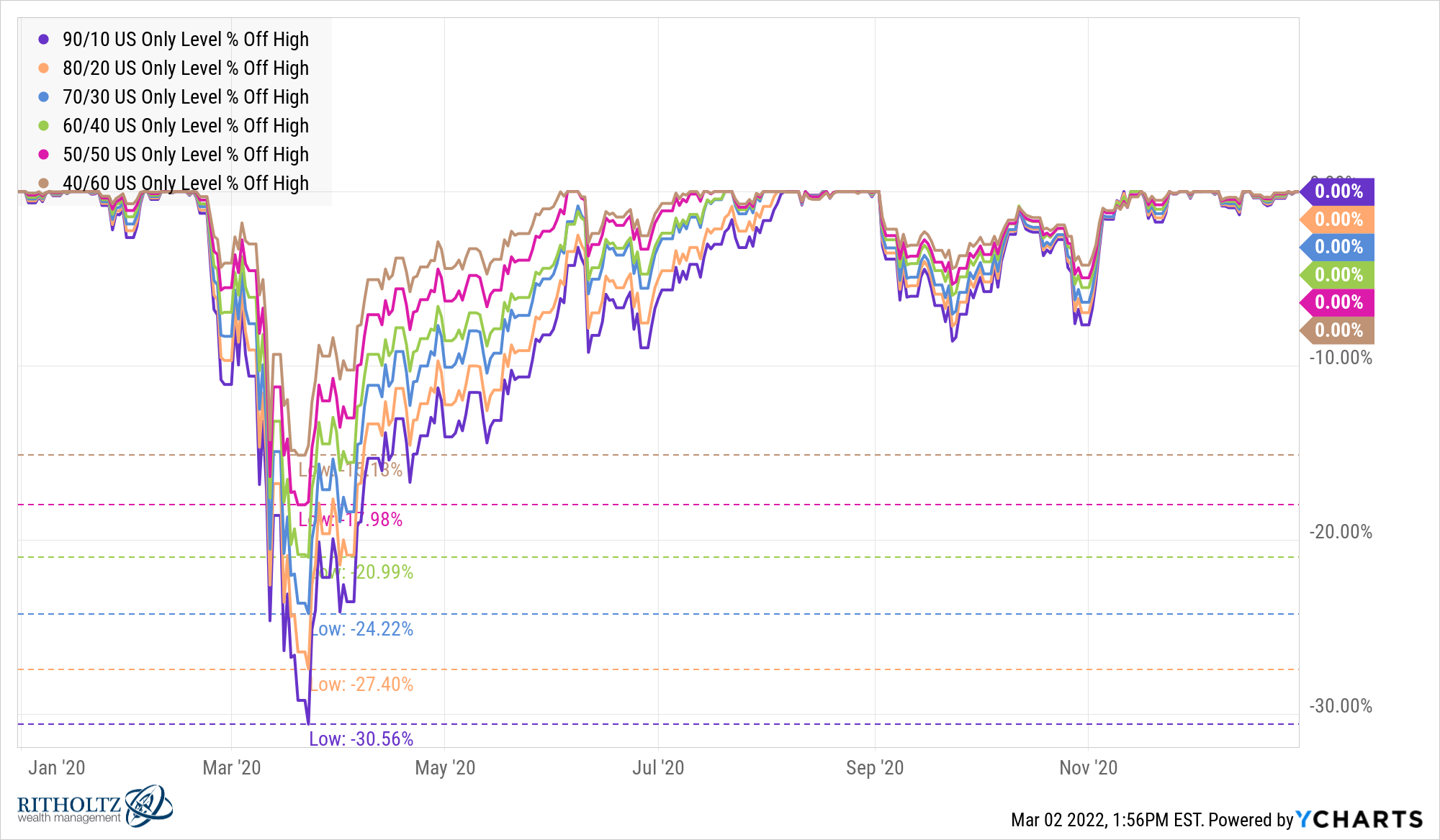

Asset allocation is important. At the start of the pandemic in early 2020, the US stock market fell about 35% in a month.

Taking some leaps in my portfolio during this volatile period certainly helped. Take a look at some of the simple asset allocations made during the crash while going from 90/10 stocks to bonds down to 40/60:

A portfolio with 40% in stocks and 60% in bonds lost only 15% in this crash while a 50/50 portfolio fell about 18%. So these more conservative portfolios did a good job of shielding investors from the downside.

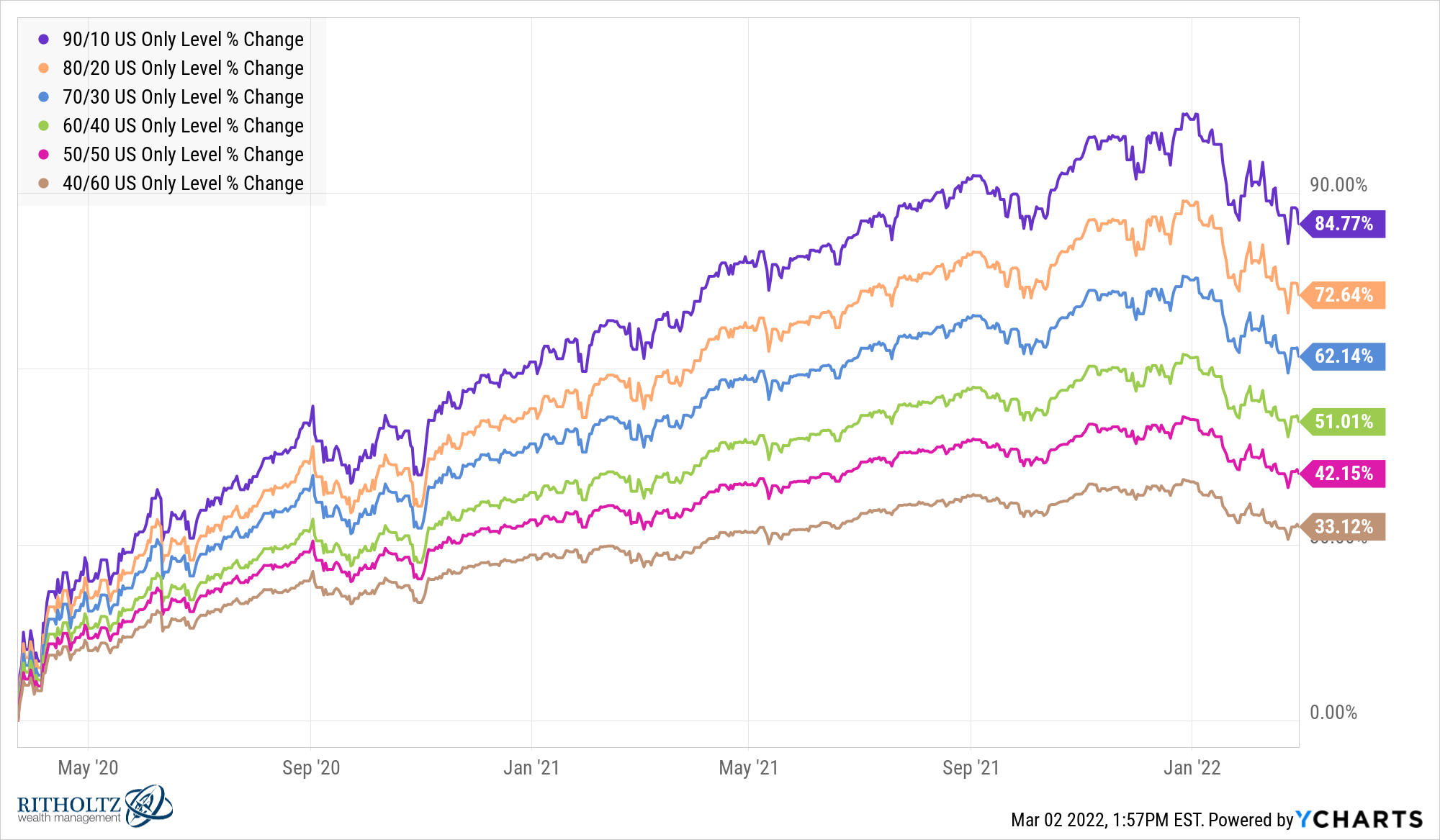

Of course, a more conservative portfolio misses out on some of the gains when the stock is rising. The S&P 500 is up nearly 96% from its March 2020 lows. The asset allocation returns for that time are as follows:

This is a trade-off when setting up your asset allocation.

More conservative funds — such as high-quality bonds and cash — tend to have lower drawdowns but lower your returns.2

And with bond yields so low, you can’t expect to earn much in terms of returns.

But investing in bonds and cash can potentially help you hedge against emotional decisions caused by stock market volatility. And while they may not provide much in the way of returns going forward, if they do help keep you alert when the stock market loses its mind, they can help reduce the odds that you might be at the wrong time. But make a big mistake.

I kept things very simple in my asset allocation examples. You can clearly diversify more than the total US stock and bond index funds I’ve used.

The key point is that your allocation between riskier assets and conservative assets can help control volatility in your portfolio and your investment decisions.

save more money A combination of low bond yields and an unwillingness to take on too much risk means you’ll probably need a higher savings rate.

A high savings rate is one of the best ways to reduce the financial risk in your life. This is one of the best ways to reduce the stress associated with making money decisions (many of which go beyond your investment portfolio).

The best part about having a higher-than-average savings rate is that it reduces your need to take risk.

Consider the location of your property. One way to balance your willingness to take less risk with the need to grow your money over time is to consider where you store your savings. Location of your risk assets can help here.

When saving for things like a wedding or a house down payment, you don’t want to take on too much risk anyway because that money will need to be spent over a few years, not decades. Those goals are ideal places for more conservative investments, like your emergency savings.

Then put your riskier assets such as stocks in a retirement account that has higher odds for bad investor behavior.

If you hide all of your stock market investments in a tax-deferred account like a 401(k), consider that money out of sight and out of mind.

Jack Bogle once said, “This is one of the most important rules of investing. If you never peek from age 20 to age 70, you’re the first 401(k) to open at age 70.” ) will rip off the statement, and I suggest you have a doctor because you will be a dead faint. Your heart may even stop. You will have so much wealth that you cannot even imagine.”

Not seeing your retirement balance is a pipe dream these days, but the idea here is to build a barbell.

On the one hand you have shorter term goals and your more conservative investments for volatility reduction. On the other end you have risky investments that you are not going to touch for decades because it will require paying taxes and a 10% early withdrawal penalty.

All you have to do is figure out what your allocation is going to be for each end of the barbell and invest accordingly.

Avoid peer pressure. The last thing you have to do is to avoid caring about how other people invest their money. Not caring is a financial superpower as it allows you to focus on your risk profile and create a plan that best suits your personality and circumstances.

Just remember, a good strategy you can stick with is much better than the right strategy you can’t stick with.

We talked about this question on this week’s Portfolio Hedge:

I also had Barry Ritholtz to discuss this question and offer some tips on how to become a better writer and communicator for your clients.

1This concept from my CFA Level III studies is probably the most important concept I learned from that Godforsaken test.