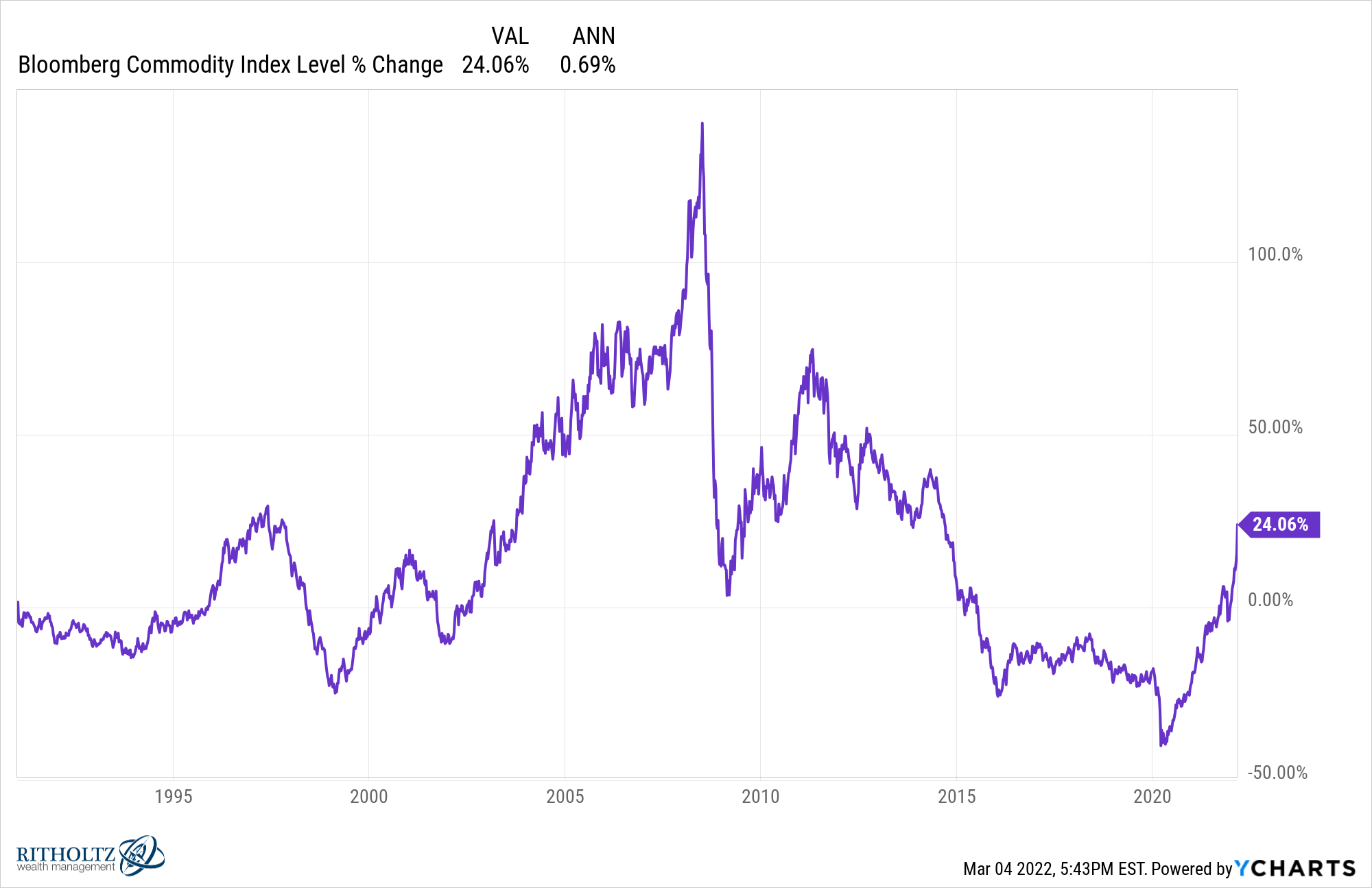

Since the inception of the Bloomberg Commodities Index in 1991, it has been up complete of 24%.

If you work hard enough, you can see an annual return of just 0.7%.

Not only is this worse than the 2.5% inflation rate at the time; This is a lower return than parking your money in cash. Three-month T-bills have returned 2.3% per year since 1991.

Even if we refer to a fully collateralized version of this futures-based index1 The return is still only 3% per year or so.

In the long term, the commodity gives you largely cash returns but with a lot of volatility.

Volatility is not good or bad. It really depends on how you react to or use that volatility.

Volatility in commodities can present both danger and opportunity, depending on where we are in the cycle.

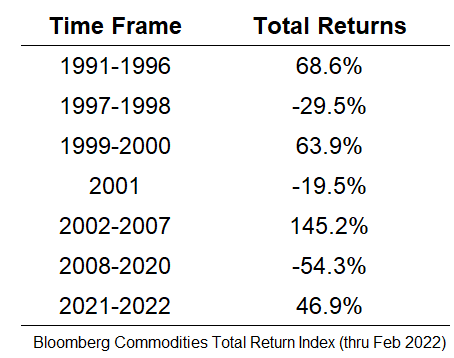

You can see the bounce-disruption nature of this asset class:

Sometimes these cycles are short. Other times they may last for an extended period.

Some think we are setting off another commodity supercycle.

It is definitely possible.

The transition to renewable forms of energy is sure to be a difficult process. As much as we are dealing with supply chain issues, the pandemic, the 2008 crisis and more than a decade after the war with one of the world’s largest energy suppliers, with little investment.

Others believe that the technology is deflationary and is bound to make prices cheaper over time, despite the current adversity.

This tug of war actually makes for interesting boom-cycles in technology and energy stocks as well.

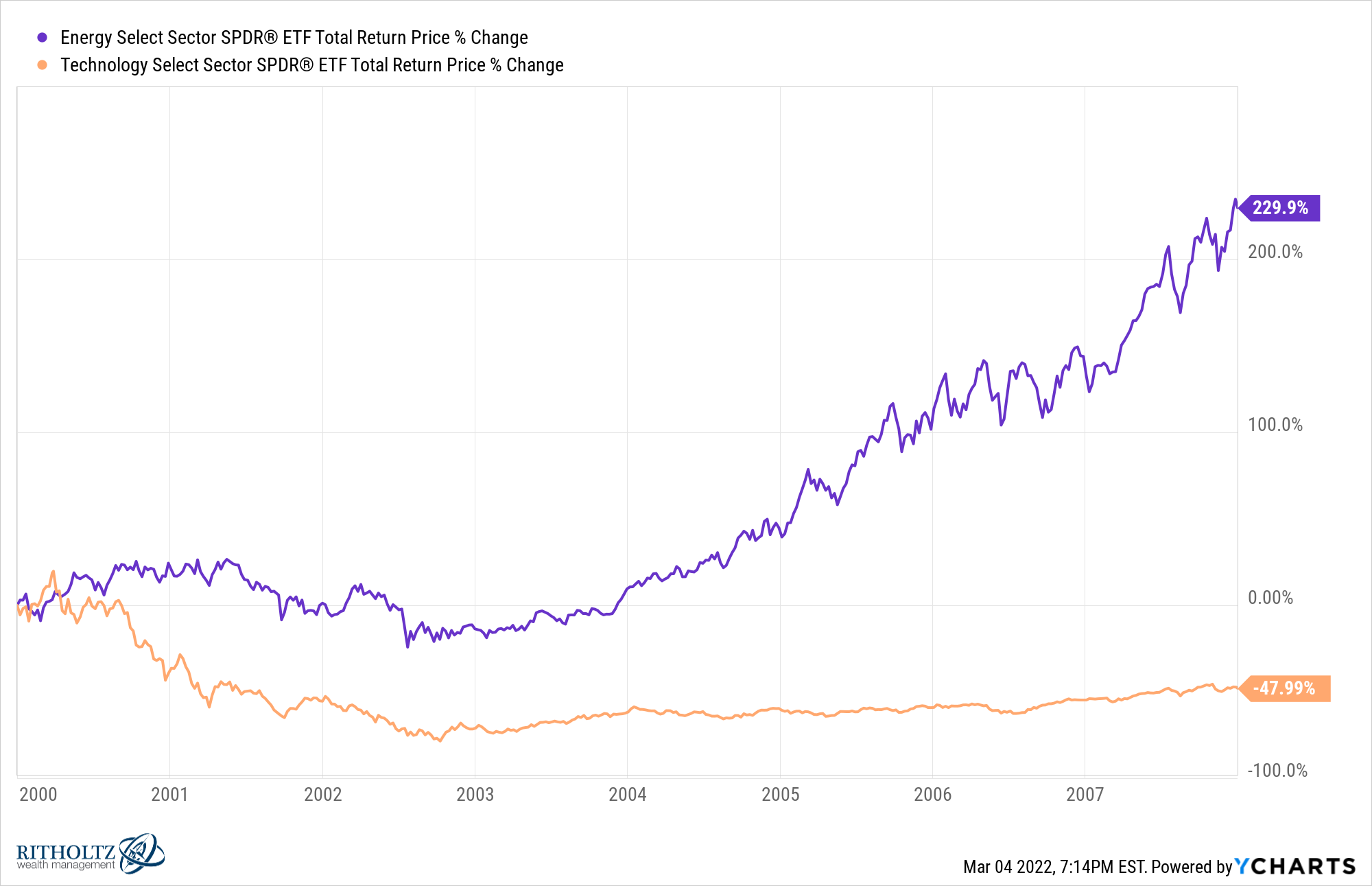

After the dot-com bubble burst, commodities went into a bull market, which saw energy stocks smoke tech stocks:

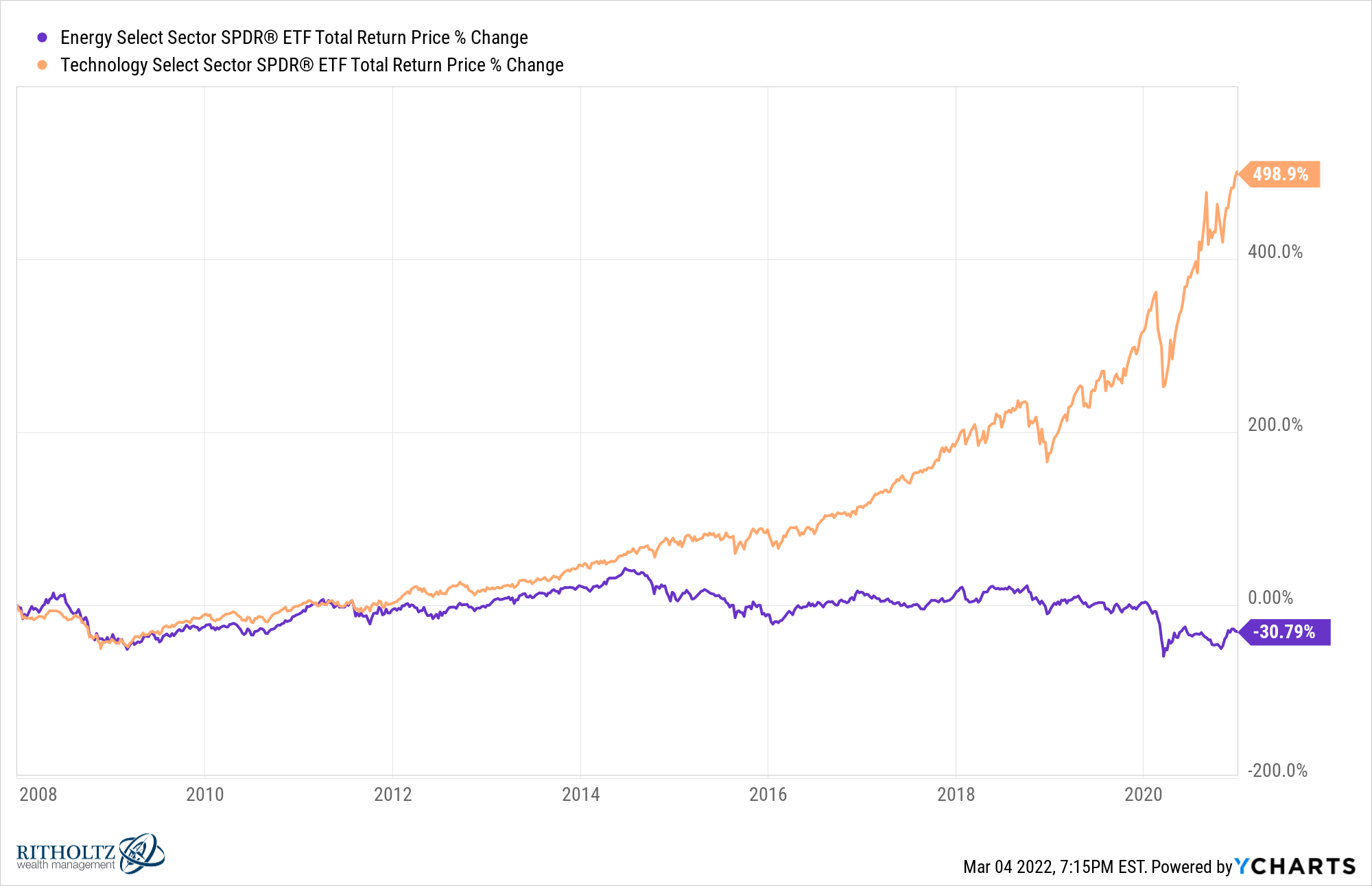

The trend was largely reversed after the Great Financial Crisis as tech stocks crushed it while energy stocks were crushed:

The highest inflation rate in four decades and a strong return to oil prices have seen energy stocks rise again since the start of 2021:

The energy sector alone has gained about 36% this year while tech stocks are down about 14%.

Despite the current rally in prices, a long bear market in energy stocks did some major damage to the sector.

In mid-2008, energy stocks made up 17% of the S&P 500. By the spring of 2020, it was down to 2.7% of the index. Even after gaining more than 100% since 2021, the energy stock is still less than the S&P’s 4%.

If you’re a fast energy stock, you can say they still have plenty of room to run after being killed for over a decade.

If you are a bearish energy stock you can point to the fact that this stuff is always cyclical and nothing lasts forever.

As with commodities, I don’t know if the energy sector will perform better. The hard part about cycles is their length and the magnitude is impossible to predict.

The problem for many long-term investors is how they react to the buoyant-dissolving nature of commodities.

After a boom in the early to mid-aughts, investors rushed to add a commodity sleeve to their allocation.

Many did this just before objects went into hibernation starting in 2008.

After years of pain, ups and downs, and losses, many investors who included commodities in their portfolios at the turn of the first decade of this century finally threw in the towel.

When it comes to cyclical investments, the worst thing you can do is buy them after all the bounce-time gains and sell them after eating a loss during a bust.

The resurgence in energy stocks and commodities combined with the downturn in tech stocks also provides a good reminder to investors who believed that tech dominance was here to stay — nothing in the markets lasts forever.

everything is cyclic.

Further reading:

Commodities are for trading, not for investing

1Fully Collateralized Index assumes that future contracts are being backed by cash which is then invested in 3-month T-bills. You can also question this index as there are many ways to look at investing in commodities.