Interest rates are moving.

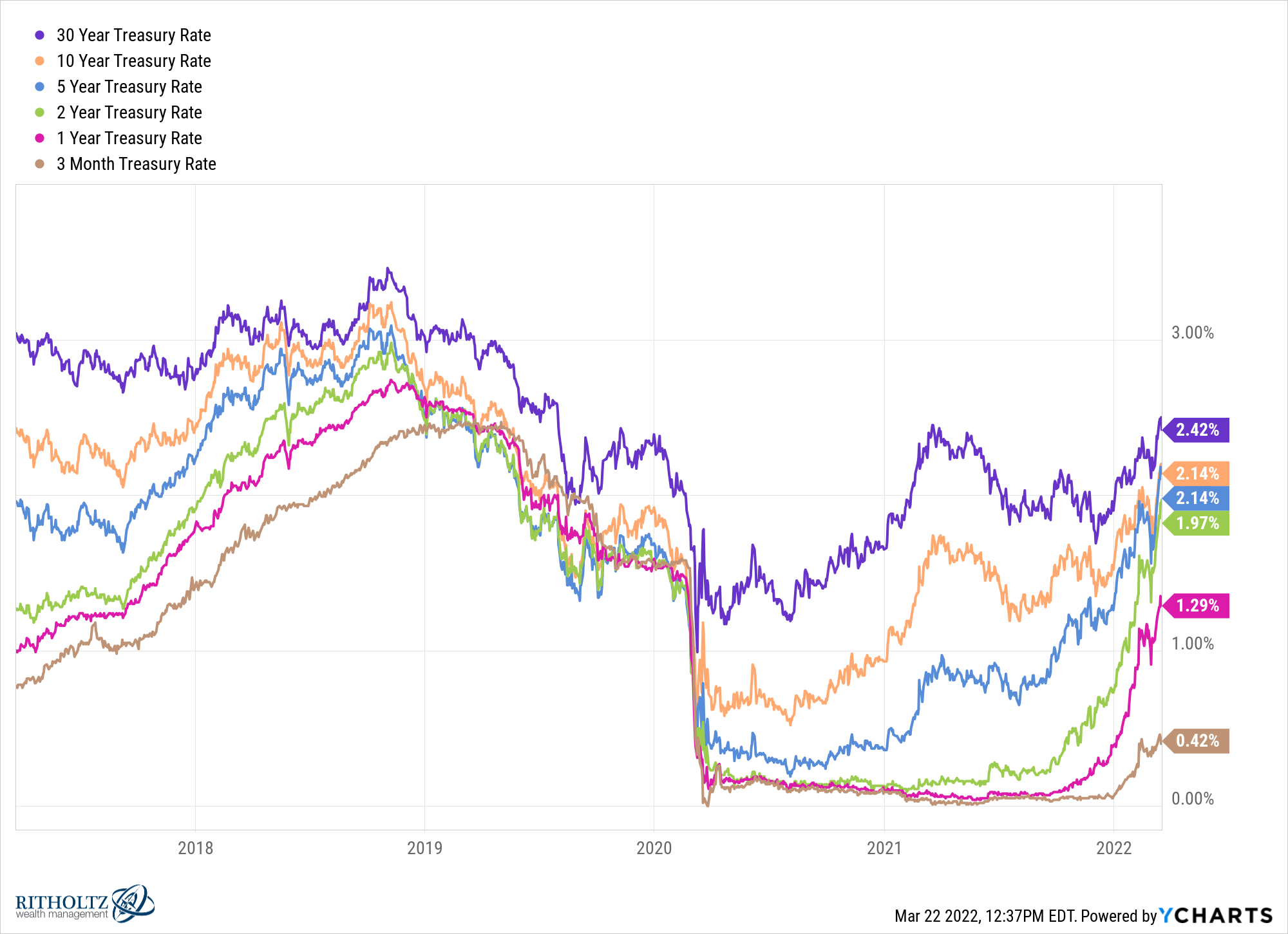

Here’s a look at government bond yields that are rising across the board:

These returns are still lower than the inflation rate, but rates are now much higher than they were a few months ago.

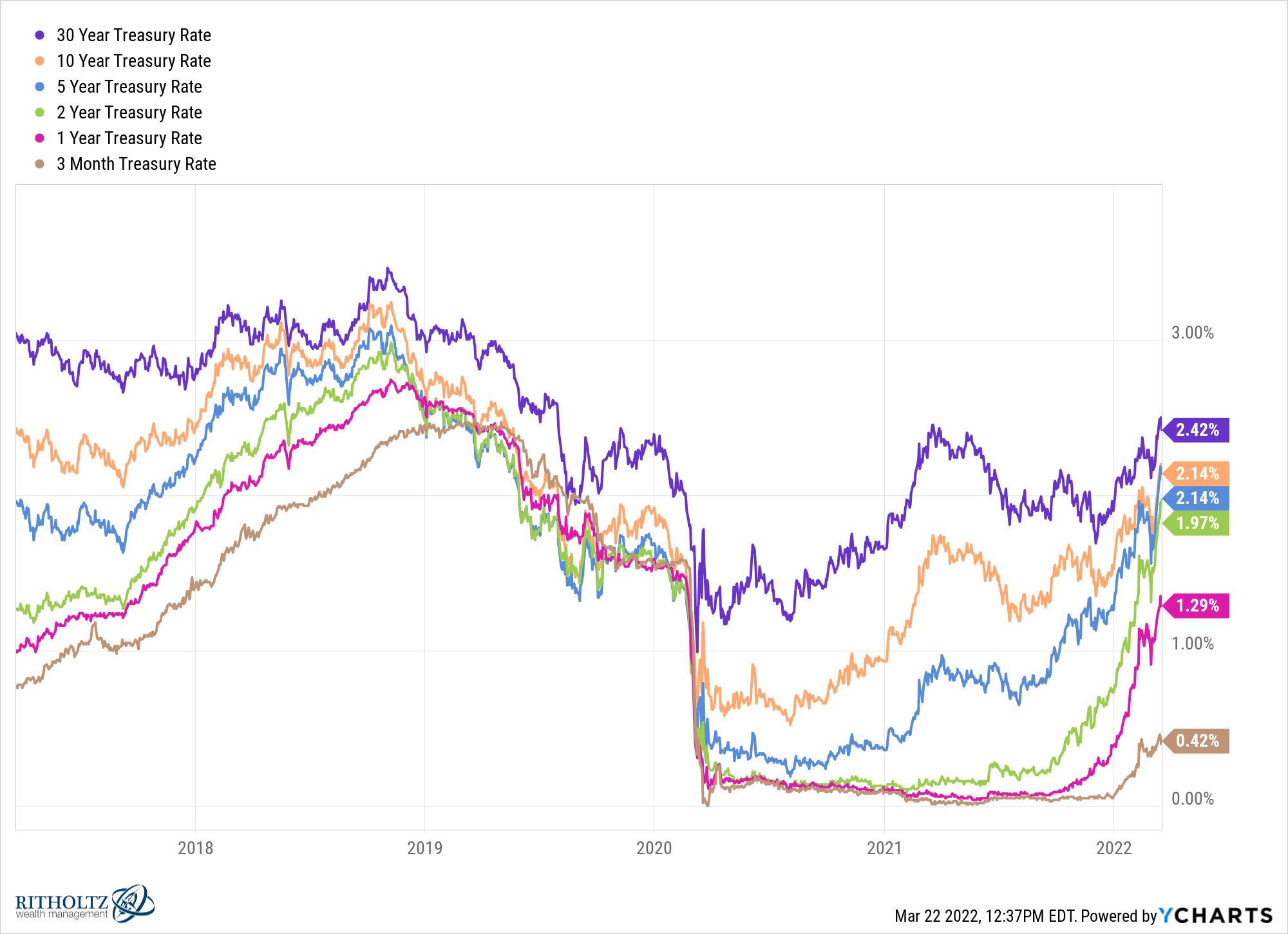

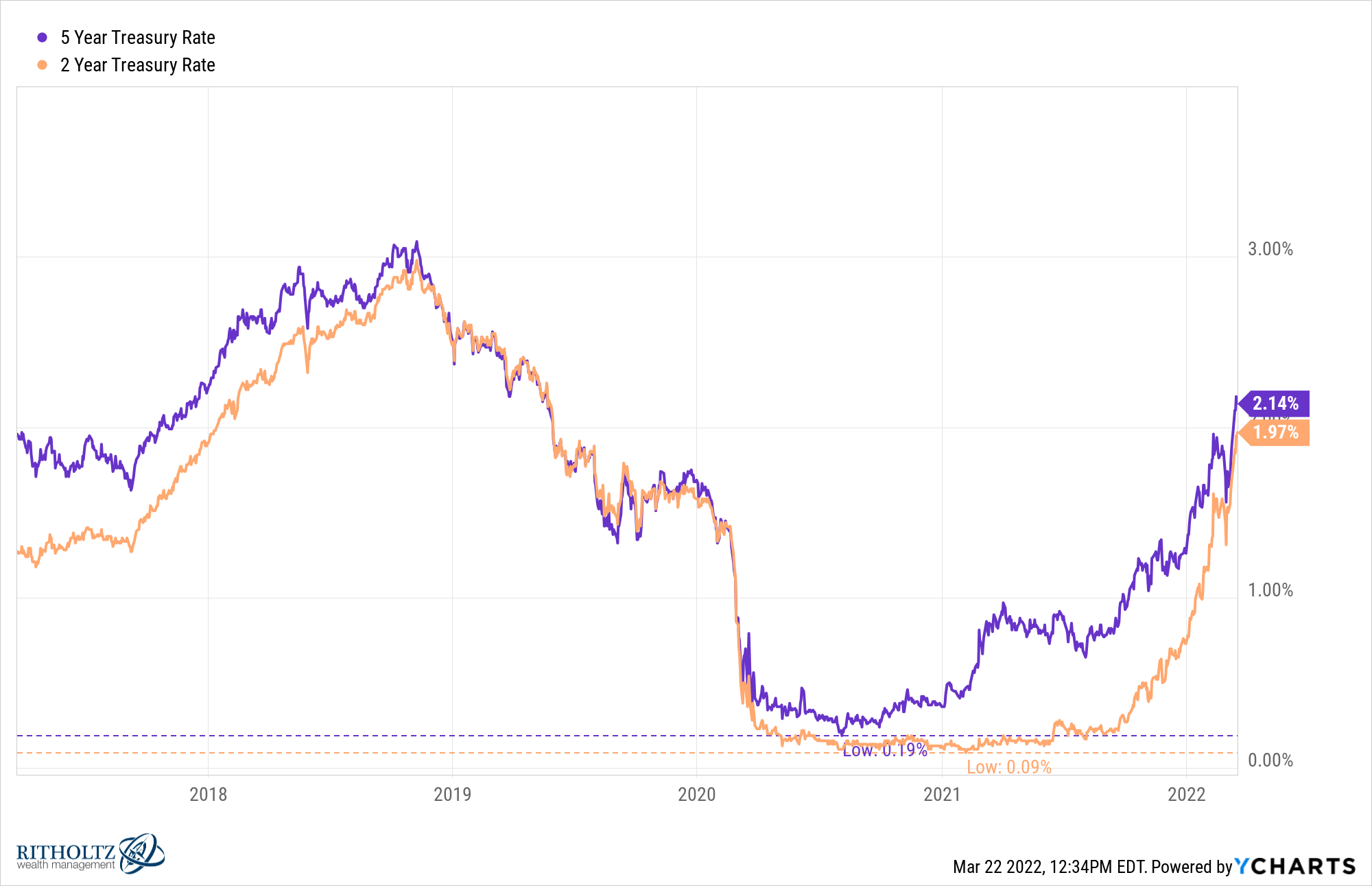

The biggest moves in terms of magnitude have come at 2 and 5 year maturities:

Both the rapid decline and subsequent rise have made quite a U-shaped move here.

It is also interesting to note that a 5 year treasury has the same exact yield as a 10 year one. The 2-year yield is not far behind.

According to the rules of risk and reward, it does not matter much that a short-term loan has the same yield as a long-term loan. This probably has more to do with the Fed’s rate hiking policy and/or more to do with the market’s outlook on the economy than anything else.

The wide spread between long-term and short-term bonds leads to an upward sloping yield curve, which can indicate healthy economic prospects – the potential for higher growth and inflation in the future. Narrow spreads lead to a flatter or negatively sloping yield curve, which can indicate poor economic prospects – most likely low growth and inflation.

Unfortunately, due to the strange economic climate we are living in at the moment, this relationship can be completely useless.

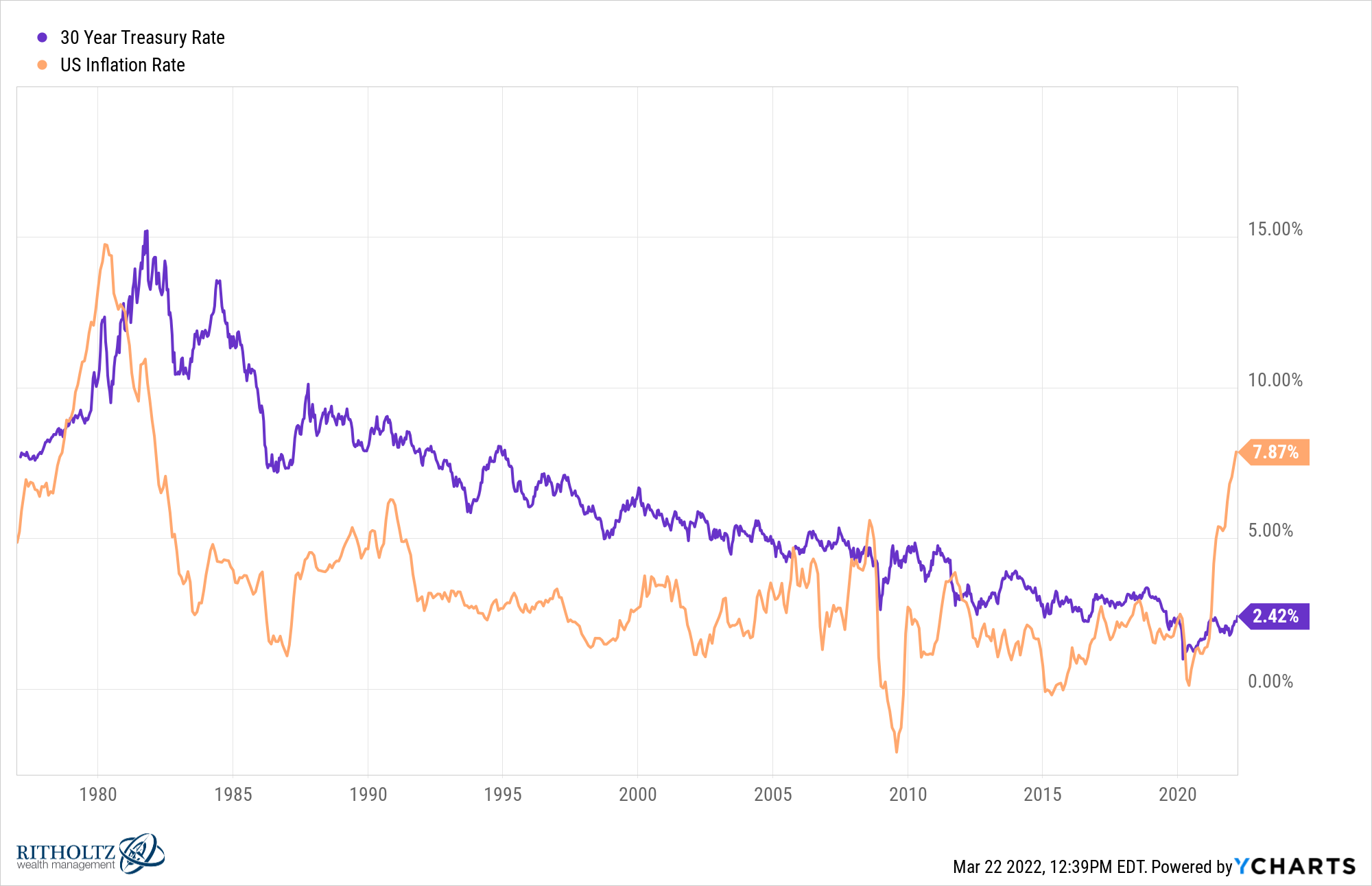

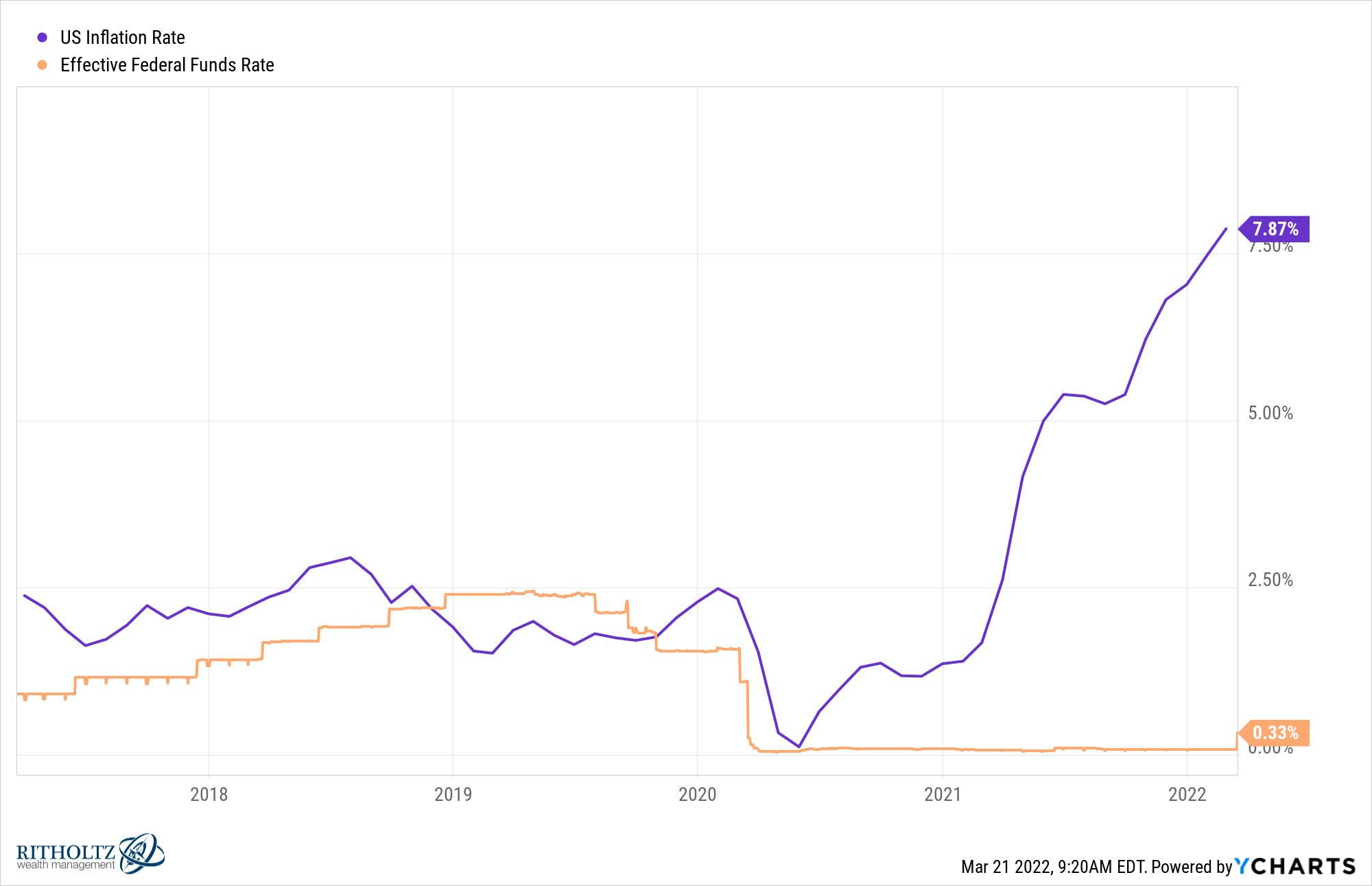

You can pretty much ruin any long-term yield chart right now by overlaying the inflation rate:

It is rare for the inflation rate to exceed the 30-year Treasury rate.

Going back to the 1970s, the highest inflation has exceeded the 30-year yield, the last time inflation was so high – in the early 1980s. In the spring of 1980, inflation was operating at more than 4% compared to the 30-year Treasury. Of course, inflation at the time was around 15% while long-term government bonds were yielding more than 10%.

At present, inflation is 5.5% higher than the 30-year yield. You’d probably have to go back after World War II to see this high prevalence. It’s certainly unlike anything investors have seen in several decades.

So what does all this mean to you as an investor?

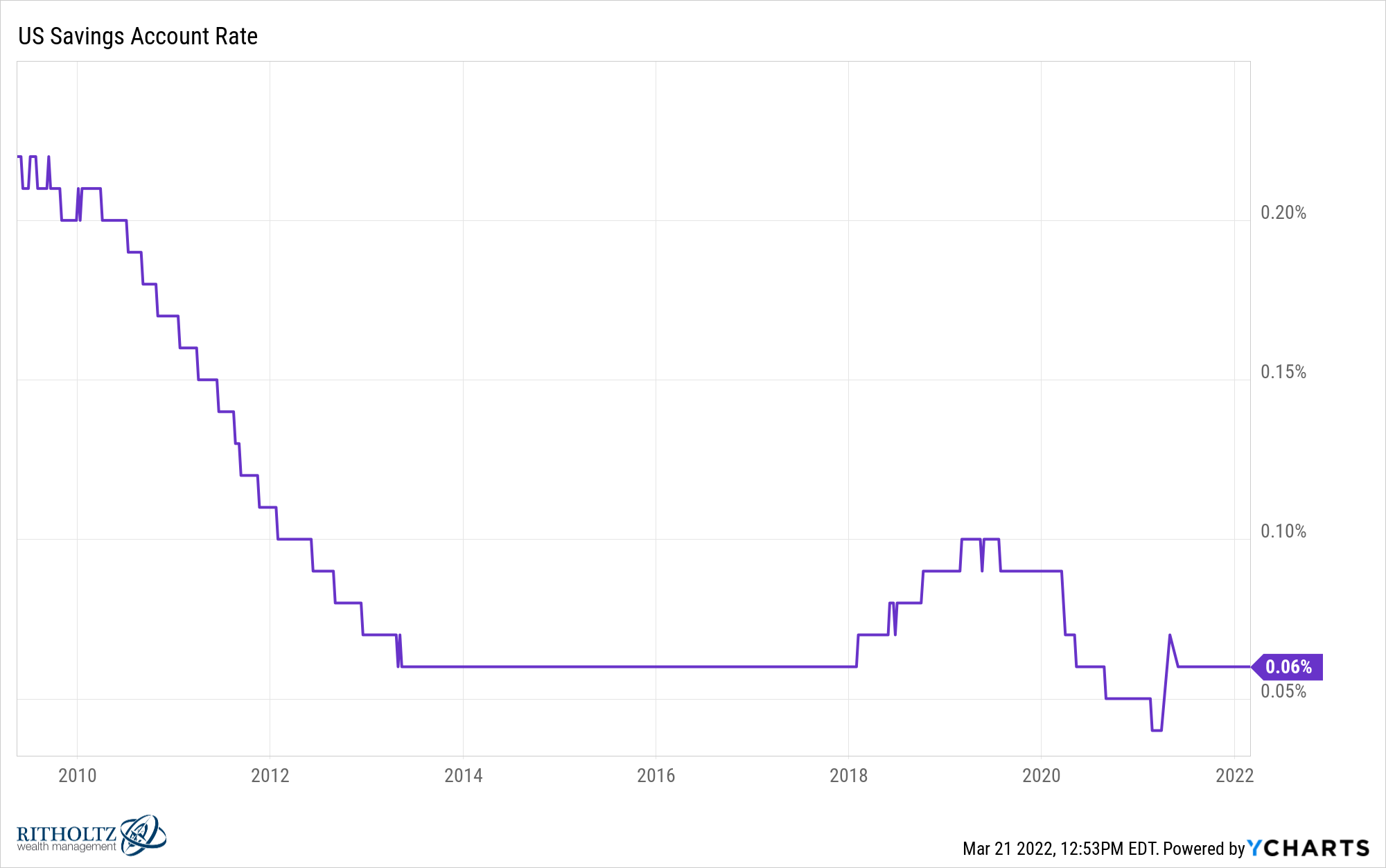

You probably still aren’t going to see much bounce in your savings account. The Fed’s talking points have helped raise yields, but they still raised their benchmark rate by only a quarter of a percentage point:

So don’t expect your savings account with brick and mortar bank to become quite high any time soon:

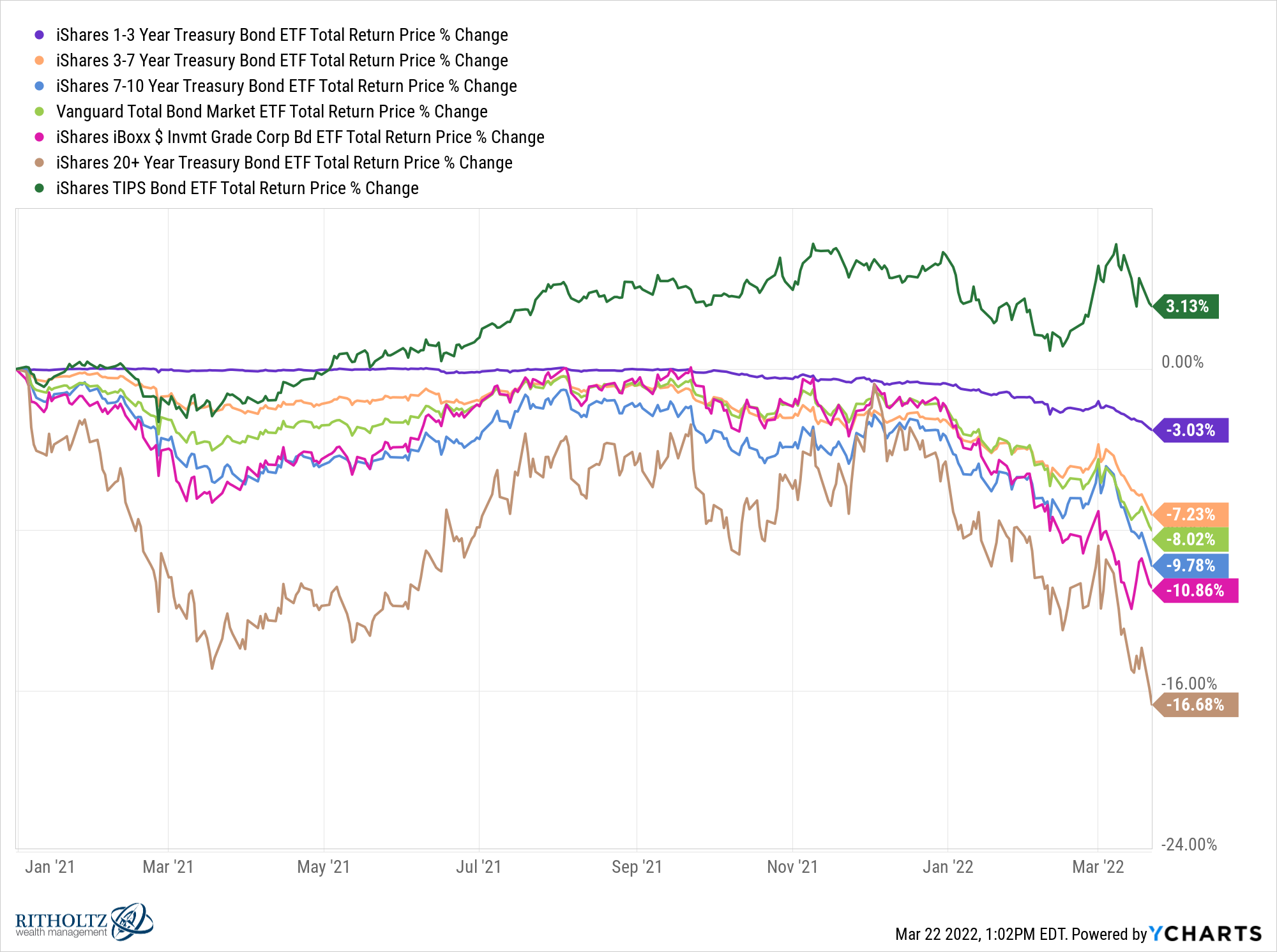

Fortunately, you can eventually get some returns in the fixed income realm. And interestingly enough, those higher returns are now in the less risky part of the bond based on volatility in the yield curve.

Take a look at the returns since the beginning of 2021 for different segments of the bond market:

TIPS have performed relatively well as inflation came in higher than expected but maturities of every other bond are down.

This makes sense when you consider that yields are inversely correlated with bond prices.

For bond investors, it’s a short-term pain for long-term gains. Higher yields mean higher returns in the future.

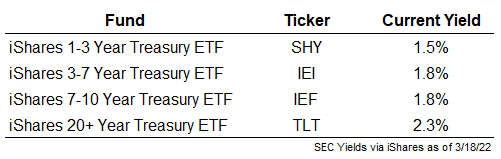

Here’s a look at the current SEC yields for various bond ETFs following the move in rates:

The general rule of thumb is that the longer the maturity and the longer the term, the more sensitive a bond is to interest rate fluctuations. This means that longer-term bonds tend to rise more when prices are lower and fall more when rates are higher.

That’s exactly what we saw.

You should also note that investors in short duration bonds are getting the same returns as those in longer duration bonds. So if rates continue to rise, you will not only experience bigger losses at the long end of the maturity spectrum, but you are not actually being compensated for that risk with a higher return.1

Bond yields at 2% are nothing to write home about, especially with inflation running at 8%. But it’s better than the rates stuck on the floor at 0%. Assuming that rates continue to rise, short-term bonds are a very good hedge against interest rate risk.

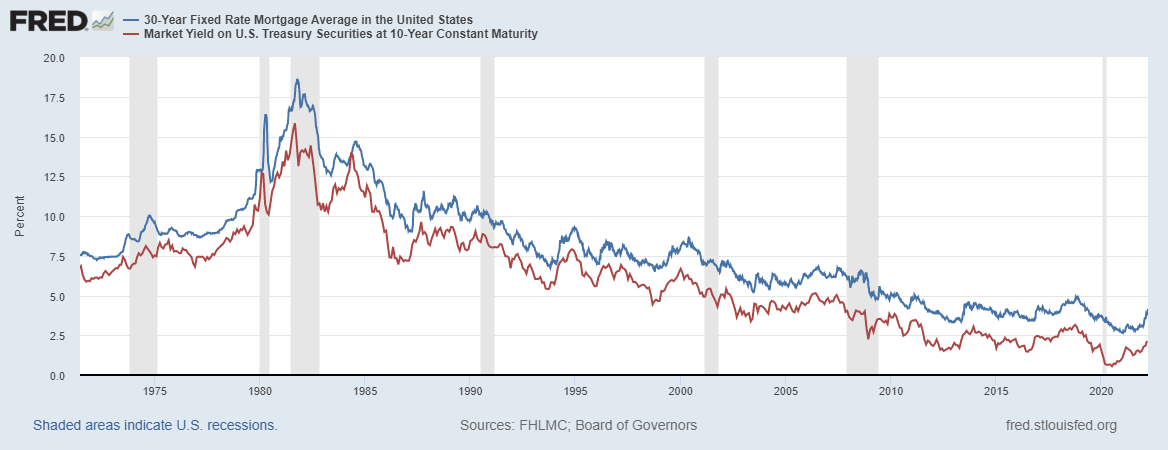

There is another side to the coin when it comes to rising interest rates – lending rates are rising.

You can see a relatively strong correlation between the benchmark 10-year Treasury yield and the 30-year fixed rate mortgage over time:

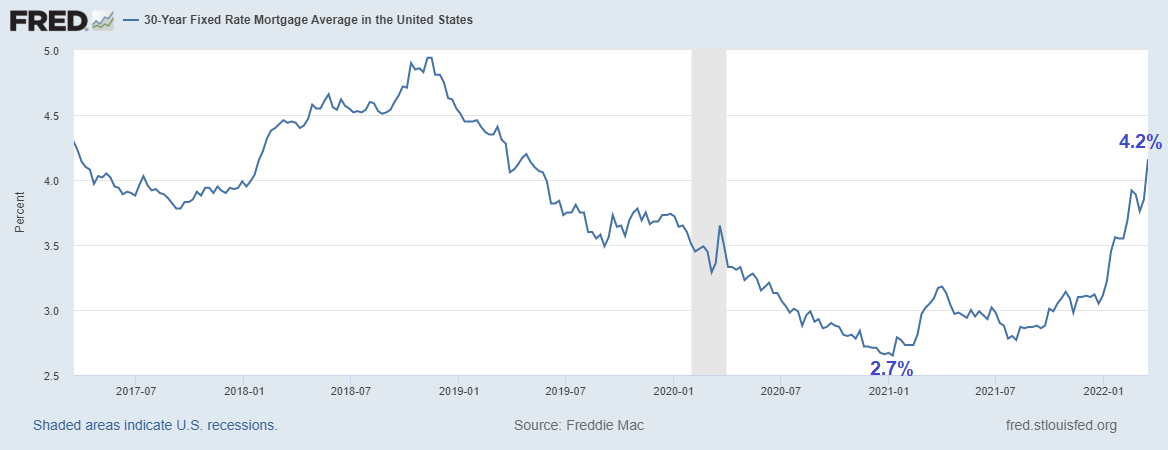

The average 30-year fixed rate mortgage came down to 2.7% in January of 2021. It was still 2.8% compared to August of last year. It is now rising further, averaging 4.2% over the previous week:

Last week’s numbers are probably already out of date. 30 years now could be as high as 4.7%.

The confluence of high inflation, high rates and high borrowing costs is going to impact investor actions at some point.

- Does it slow down the crazy housing market?

- Does it make the housing supply problem worse if people don’t want to trade in for a higher mortgage rate?

- Will investors now put more money in bonds if yields are higher?

- Or will investors now pull money out of bonds because they have suffered some loss?

- Do stocks still rule the day when real bond yields remain firmly in negative territory?

These actions are happening so fast that it is difficult to know what will happen.

All I know is that things get weird when it comes to both the economy and the market.

We are all dealing with environments we have never experienced before.

Further reading:

Why would anyone have bonds right now?

1Obviously, if rates fall, longer-term bonds will yield higher returns from price fluctuations.