This article was originally published on LinkedIn

RIA Group-Think has been a supporter of consolidation for the past decade, and is increasingly doing so. You’ve read the headlines about the pace of deals reaching a fever pitch last year and continuing this year. We have been skeptical of the trust requirement for RIA consolidation in this blog in the past, and have not deviated from our position yet. But opinion is only opinion, and facts are facts. It seems like an opportune moment to check our feelings against reality.

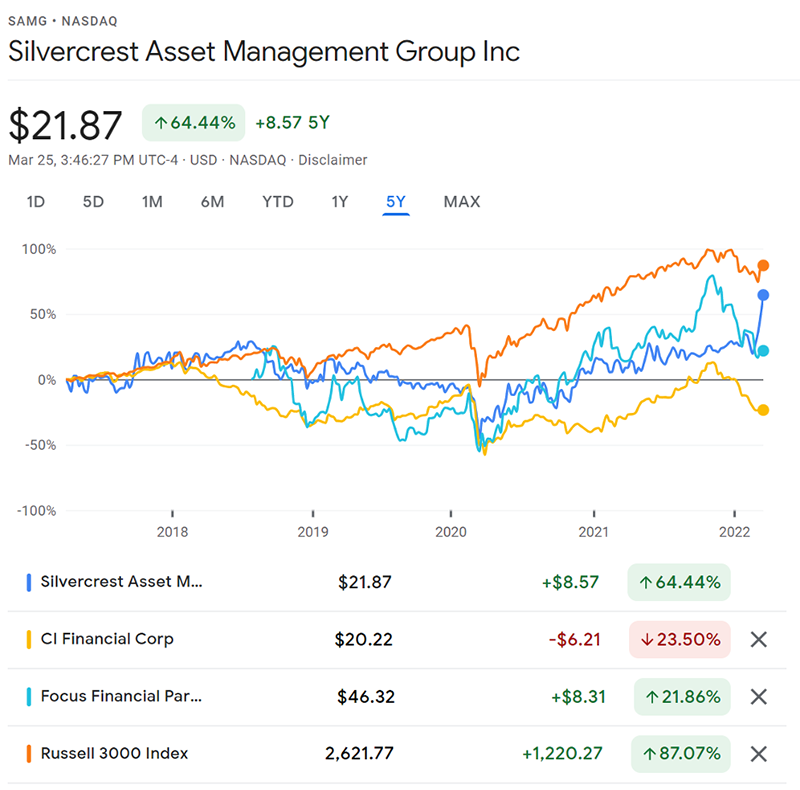

How is the integration of RIA performing so far? The verdict of the public markets is not very encouraging. We looked at three publicly traded consolidators of wealth management businesses: Silvercrest, CI Financial and Focus.

Over the past five years, Silvercrest Asset Management Group (SAMG) has shown cumulative share price appreciation of less than 65%, outperforming the Russell 3000 by more than 2,200 basis points. To be fair, SAMG pays a fair dividend, and its wealth management clients probably don’t invest 100% in equities. Nevertheless, we believe that RIA returns are being leveraged for the market, and in an era of strong markets a wealth management firm with organic growth and an acquisition strategy should – in theory – be able to outperform the broader indices. .

SAMG didn’t beat the market, but it outperformed some rivals. Despite the tremendous number of acquisitions and sub-acquisitions, Focus Financial Partners trades at less than 25% of its IPO price since the summer of 2018. Focus does not pay dividends, so that 22% cumulative return to FOCS shareholders is a total (total) return since going public. CI Financial has done even worse, as the Canadian shop respected for its willingness to pay top dollar hasn’t posted a positive return over the past five years, regardless of where you count the dividend.

Keep in mind, all of the above happened in an era of strong equity markets and low interest rates – which should be optimal conditions for the RIA space to consolidate.

essential car story

The business environment of the late 1990s was such that consolidation prevailed in almost every industry. Rollup IPOs were the SPACs of the day, with newly minted dot-coms trading their highly inflated equity currencies for the highly inflated equity currencies of other companies, and old economy makers working together to share branding, technology and overhead. were. Sometimes it worked great, and sometimes it didn’t.

It is often said that most M&A results in failure. The free-wheeling, mass-market managers at Chrysler couldn’t match up to expectations with the hierarchical, engineering-led team at Daimler-Benz. Loveless marriages resulted in unfortunate offspring like the Pacific Crossover and the R-Class. Less than a decade after the 1998 merger, Daimler offloaded Chrysler to Cerberus for about 25% of the $36 billion it had originally paid for.

At the same time, a more unlikely pairing actually worked. The sale of Lamborghini to Volkswagen’s Audi division in 1998 was a huge success. Italian styling and German build quality make a good combination, and today Lamborghini sells for almost fifty Many times more cars are bought annually by Audi than before. It hasn’t caught up with Ferrari yet, but it’s close enough for the folks in Modena to notice.

investment thesis

Looking back on the two auto industry transactions sheds some light on the expected performance of the RIA deals. One way to compare Daimler-Chrysler and Audi-Lamborghini is to consider why They came in first place.

Daimler-Chrysler was a bulked-up, bigger-is-better, merger-than-equals. The argument was driven by internally focused economies of scale, and it was unclear who was in charge. This left an environment that was unusually hospitable to cultural conflicts that eroded opportunities, synergies and (eventually) sales.

Audi-Lamborghini was product-focused, and from the start it was clear who got what. The huge growth in Lambo’s sales and the opportunity with Pruning Horse to equal or surpass its old rival kept internal discontent at bay.

Which transaction most closely resembles the typical RIA transaction? investment thesis for investment in RIA (whether asset management or wealth management) is straightforward: sticky revenue and operating leverage produce a sustainable coupon with the tailwind of the market. In the era of ultra-low yields, this is one of the best growth and income trading options available, and it has become a crowded business with a wide variety of institutional investors and family offices. As we have said many times in this blog, it is easy to see why one would invest in investment management.

consolidation thesis

Investing in an RIA is one thing; Integrating them is another matter entirely. Still, the topics driving industry consolidation are equally defensible:

the measure, With 15,000 or more RIAs in the United States alone, the solution to fragmentation seems like an obvious play. Consolidation conquers all the financial leverage that comes with economies of scale, increasing margins, distribution and value.

the access, Larger firms can theoretically source more sophisticated investment products, technology stacks and marketing programs.

problem solving, There should be an incentive for sellers to relinquish control of their own destiny, and consolidation is often seen as a solution to aging leadership (or at least aging ownership) without a compelling succession path.

financial engineering with loans, Covenant-light loans at lower rates have made capital available to public and private acquirers alike. Banks will typically lend up to 3x and non-bank lenders up to 6x. With LIBOR near zero, yield premiums on the order of 500 to 600 basis points also make LBOs attractive.

Financial Engineering with Equity. Multiple arbitrage has been a slave to cheap credit. At one point, it would “buy at five to six times, sell at eight to nine times.” Then the spread was 9 to 12. Then it was 12 to 15. Then it went ahead. Whisper numbers usually outweigh reality, but the logic is the same.

All of the above are widely accepted in the industry, and it’s easy to see why. But if Fed activity throttles equity markets, as well as raises borrowing costs, things could suddenly change. Not only would this threaten the consolidation of the industry for financial reasons, but it could also expose some of the flaws in the consolidation thesis.

scale discrepancies

If you put together ten RIAs, each of which generates $5 million in EBITDA, your combined operation would create $50 million in EBITDA. Your holding and management operations, however, will likely require a C-suite, an accounting department, a marketing department, legal, compliance, investor relations, and an executive team with a few pilots for your jet. All of them will need office space in a good building, even though they mostly work from home. Monitoring costs will inevitably lead to overall profitability.

Some of this expense may replace tasks that previously took place at the subsidiary RIA level, but not all of them. Is there enough expense synergy in the consolidation to cover the overhead costs of a consolidator? I doubt

In the asset management space, there is an argument that AUM can add up faster than overhead, and margins can expand almost infinitely (we’ve seen a few large ones). In money management, this is a tough slow. When Focus Financial went public, we thought that, even with the massive growth, it would be hard to get their adjusted EBITDA margin above 25% — a level we’ve come to report among wealth management firms of a comparatively modest proportion. are accustomed. A publicly traded consolidator may have more than 100 souls at the management company level. That’s a lot of payroll to cover with an assistant-level cadence.

easy use

Are small firms left out when it comes to essential products and services? With custodians eager to accommodate all types of investment products, outsourced compliance, subscription-based technology and scalable marketing, it is easier than ever to compete as a sub-billion dollar RIA. Scale enables firms to provide positions to manage these functions, but it does not provide the functions themselves. We’re not experts in RIA operations, but we’ve yet to see a small resolute struggle because it couldn’t get what it needed (or wanted).

exit and succession

Consolidators offer exit capital for RIA founders. In that regard, they can resolve the impasse between generations of leadership and pay senior members a price that the next generation of employees either cannot or will not pay. But a cheaper source of capital (or a greater appetite for risk) is not a surrogate for inheritance.

Since most integrators are relatively new to the industry, we don’t know much about whether these models are sustainable. RIAs are not capital intensive, but they rely heavily on employees to manage both money and relationships. Often the employees who will generate returns for the consolidator in the future do not get a very high equity return in the transaction. And will the founding generation work as hard for their new owner as they did for themselves?

These complications have prompted many consolidators to structure earnings or develop hybrid ownership models that share some form of equity return with subsidiaries RIAs. A broker promises to “never turn an entrepreneur into an employee” – which sounds reasonable. Ultimately, however, employees of subsidiary operations are sharing equity returns with the parent company, and the principal/agent dilemma can be less of a dichotomy and more of a spectrum.

As such, the consolidator would pay for a firm created by highly motivated founders and obtain a firm that would eventually be run by differently motivated successors. RIA consolidation is the act of simultaneously acquiring an inherited operating asset and acknowledging pro forma succession liability.

Financial De-Engineering

Most RIAs, by far, operate on a debt-free basis. Typically, this is the obvious reason why there isn’t much of an asset base to finance, so why bother(?) On the other hand, consolidators often rely on debt financing and leverage ratios as deal prices have risen. are also. Financing a cash flow stream that is leveraged in many ways to Fed activity works very well in an era of decline and low interest rates — as we’ve seen.

Rising rates and falling (or stagnant) markets result in a higher debt burden and less cash flow to service that debt. Along with this, increasing inflation risk has increased the payroll burden. In normal times, there would be enough equity cushion to guard against default. With high deal multiples — based on highly adjusted EBITDA measures — and the massive leverage available from non-bank financing, we could be in for some pretty surprising surprises.

If coverage begins to weaken, deal activity will stop and multiples will drop. If the multiples decline, the acquirer will not be able to exit on satisfactory terms. Without equity compensation in the form of a carrot, high performers would find an exit for themselves. The unfortunate reality of leveraged RIAs is that their assets get on the elevator and go home every night, but liabilities never leave.

Climate change

I’m not saying the end of the RIA consolidation trend. For a variety of reasons, this may continue for years to come. But publicly traded consolidators have underperformed despite the favorable conditions in which those business models should flourish. Now that we have the prospect of an RIA stagflation downturn, it can be very difficult to maintain a land-grabbing mindset and act as if acquirers are valued on a cost-per-press-release basis.

Matt Crowe is the President of Mercer Capital